Current AI economic and technological assumptions are about to change dramatically. As Nebari enables everyone to have their own intelligence hub, we have to re-think AI.

A Strategic Framework for World Leaders

By Joe Merrill

Artificial intelligence is entering its infrastructure phase. Today’s global market favors large foundation models, hyperscale data centers, and centralized compute. That preference is rational given current benchmarks and capital flows.

However, it is incomplete.

The next phase of AI competition will not be determined solely by model size. It will be determined by ease of use, orchestration, energy efficiency, and control of inference across distributed systems for higher fidelity at global scale.

Large models will remain essential. But they will not remain dominant for every task. Nations and enterprises that assume scale alone guarantees superiority risk overinvesting in centralized infrastructure while underinvesting in distributed intelligence that is easy to use.

This outline does not argue against frontier models. It argues that frontier models are not the final architecture.

I. The Current Market Logic

The present AI economy rests on three defensible assumptions:

Centralization simplifies governance and security.

These assumptions are supported by scaling laws and benchmark performance. Frontier models demonstrate remarkable cross-domain capability.

But general capability is not the same as economic optimality and high fidelity.

Most enterprise and governmental AI use cases are bounded:

Fraud detection

Logistics optimization

Energy forecasting

Compliance automation

Defense modeling

These tasks require precision within domain constraints. They do not require universal reasoning engines.

The central question is no longer:

Who can train the largest model?

It is:

Who can deliver optimal inference at sustainable cost and sovereign control?

II. The Immutable Law of Tensor Data

The Immutable Law of Tensor Data: For any AI inference problem, there exists an optimal quantity and structure of information required for accurate tensor inference. Data beyond this threshold introduces inefficiency, noise, or spurious correlation.

This is not a rejection of scaling laws. It is a refinement of them.

Scaling improves generalization when the task is unknown. But when the task is known, excess context can:

Increase energy consumption

Introduce irrelevant correlations

Reduce interpretability

Increase attack surface

Inflate cost

The future advantage belongs to those who know:

What information is necessary

What information is irrelevant

How to structure data for optimal tensor efficiency

The race is not for the largest model. It is for the most efficient, high-fidelity signal.

III. The Role of Large Models in Future Architecture

Large models will remain critical for:

Frontier reasoning

Multimodal synthesis

Model distillation

Bootstrapping domain systems

They are analogous to supercomputers in the 1980s. Essential. Specialized. Powerful.

But they will not be the operating layer of global AI.

Over time, most production workloads will shift toward:

Smaller domain-optimized models

Routed model architectures

Edge inference systems

Hybrid compute clusters

The winners will orchestrate across model sizes, not bet exclusively on one.

IV. Lessons from Distributed Computing

In the late twentieth century:

Supercomputers built by Cray remained essential.

But distributed personal computing, enabled by Microsoft and Intel, reshaped the global economy.

Centralized compute did not disappear. It became one tier in a layered system.

The transformative shift came from:

Standardized operating layers

Modular hardware ecosystems

Distributed deployment

Lower barriers to participation

AI is approaching a similar inflection.

V. The Strategic Vulnerability of Hyperscale-Only Thinking

Hyperscale infrastructure carries real strengths:

Economies of scale

Rapid iteration cycles

High hardware utilization

But it also introduces structural risks:

Energy concentration

Supply chain dependence

Geopolitical leverage imbalances

Latency bottlenecks

Data sovereignty conflicts

Single point of failure security

Centralization optimizes for providers. Distributed orchestration optimizes for users and nations.

Resilience, cost and fidelity increasingly matters more than scale prestige.

VI. Orchestration as the Decisive Layer

The core strategic question is not large versus small models.

It is:

Who controls orchestration across heterogeneous models and distributed compute?

OpenTeams’ Nebari provides:

Model lifecycle management

Multi-model routing

Sovereign deployment environments

Distributed compute orchestration

Integration across public, private, and edge systems

Nebari does not replace frontier models. It integrates them.

Just as operating systems abstracted hardware complexity, AI operating layers will abstract model heterogeneity.

The dominant power in the AI era will not be the largest model builder. It will be the orchestrator of inference.

VII. Addressing Common Objections

“Frontier models outperform small models.”

True in general benchmarks. False in most bounded enterprise contexts, research, and science.

Performance must be measured relative to task constraints and cost.

“Distributed systems are more complex.”

Without orchestration, yes. With standardized orchestration, no.

Complexity migrates from the user to the platform.

“Hyperscalers can integrate orchestration themselves.”

They will attempt to.

But sovereign environments require:

Cross-cloud interoperability

On-premise integration

Air-gapped deployments

National control layers

No single hyperscaler can credibly serve every sovereign boundary without conflicts of interest.

The opportunity lies in neutral orchestration.

“Capital markets favor hyperscale.”

Markets often overconcentrate in infrastructure cycles. Telecommunications, railroads, and fiber optics all experienced this pattern.

Distributed optimization historically follows central buildout.

VIII. Implications for Data Centers

Data centers will not disappear.

They will evolve toward:

Regional clusters

Energy-proportional scaling

Edge compute augmentation

Hybrid public-private orchestration

Instead of monolithic GPU concentration, we will see federated compute networks.

Energy economics will drive this transition.

IX. Strategic Guidance for Nations

World leaders should pursue dual-track strategies:

Maintain access to frontier model capability.

Invest aggressively in distributed orchestration and domain models.

True sovereignty does not mean replicating hyperscalers.

It means controlling inference pathways, data governance, and energy exposure.

X. Conclusion

The current AI paradigm is not wrong. It is incomplete.

Large models expand possibility. Distributed orchestration secures sustainability. Small models are the path to efficient fidelity.

The Immutable Law of Tensor Data reminds us:

Intelligence is not maximized by volume alone. It is maximized by relevance and structure.

The coming era will reward those who:

Optimize signal over scale

Distribute rather than concentrate

Orchestrate rather than centralize

Build resilience rather than prestige

History does not eliminate centralized systems. It absorbs them into distributed architectures.

AI training and deploying companies are trying to capture your data. An understanding of the industry economics can help you avoid this pitfall.

Artificial Intelligence (AI) is often framed as the domain of a few elite companies. But a closer look reveals a massive gap between those who actually build AI and those who put wrappers on it, train it, and resell it.

The actual numbers for who builds AI are shockingly small. Only a small number of companies, primarily five, contribute to open-source AI at scale: Meta, Google, Nvidia, Microsoft, and OpenTeams. In saying so, I also want to point out smaller and significant contributions from companies like Stability AI, EleutherAI, and Mistral, who all make meaningful code updates and changes despite their smaller size.

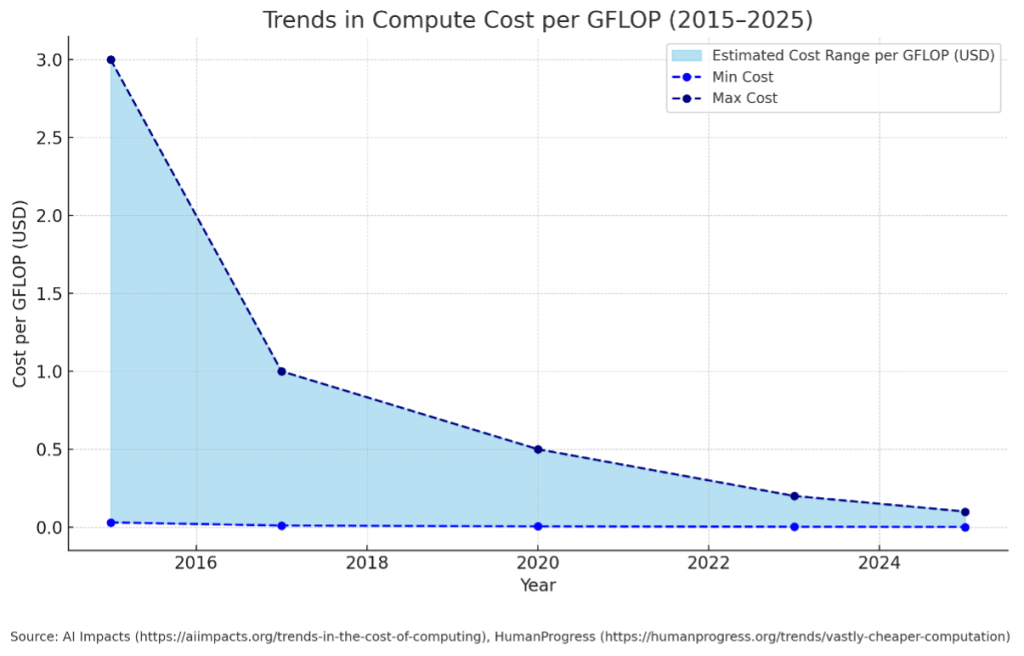

Because open source AI is free to download doesn’t mean it is free to operate. Like adopting a puppy, you still have non-trivial startup costs and maintenance. However, these expenses are not what industry developers have traditionally suggested and are shockingly affordable for most enterprises.

These economic factors combine to produce an AI industry with barriers ironically related to human development and not compute. Just as the best time to plant a tree is 20 years ago, the best time to create new AI developers was a long time ago. It will take a generation to produce adequate supply for the field due to lengthy training requiring PhD level know-how in mathematics, statistics, and computer science plus years of coding experience.

On the technical input side of the AI building equation, training costs are collapsing and with an increasingly high-quality library of pre-trained, open source models already available, everyone can have their own AI. Indeed, those who don’t will be at the mercy of those who do.

Shareholders and voters will not buy the story that giving away their competitive and personal data to AI oligarchs is economically necessary or valuable. Communal LLMs are economically inefficient, epistemically noisy, and strategically reckless for any enterprise or government that values performance, accuracy, or control of its intellectual property. The privacy risks inherent in communal models are real. The future of AI will be enterprises owning their open source AI to save costs, provide accurate answers, and protect their intellectual property. This is the efficient market solution preferred to communal LLMs sucking massive power to untangle spurious correlations from superfluous data.

To be sure, black-box AI SaaS providers will still have a business model as “drivers” of AI as opposed to those who build and deploy it. However, that economic pie will be smaller just as F1 drivers still do financially well, but nowhere near the economic returns earned by those who build cars. The upstream builders of AI will always have an advantage when deploying and training models because of the advanced know-how they possess to optimize AI and fully take advantage of its capabilities.

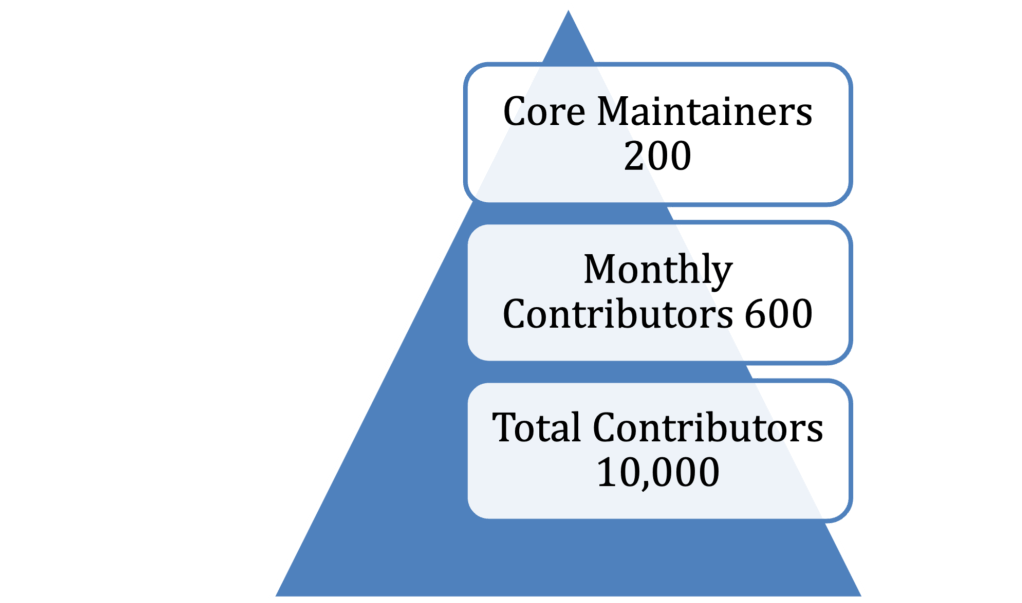

The AI Industry Pyramid

Below is a visual representation of the AI workforce, from elite maintainers to the broader ecosystem of users:

Detailed Platform Stats

1. PyTorch – GitHub contributors: ~3,900+ – Monthly active contributors: ~250 – Core Maintainers: 80 – Users: ~4–5 million – Lead Developer: Meta AI – Source: https://github.com/pytorch/pytorch

2. TensorFlow – GitHub contributors: ~3,500+ – Monthly active contributors: ~200 – Core Maintainers: 70 -Users: ~2.5–3.5 million – Lead Developer: Google – Source: https://github.com/tensorflow/tensorflow

3. Hugging Face – GitHub contributors: ~2,600+ (Transformers repo) – Monthly active contributors: ~150 -Core Maintainers: 50 – Users: ~1.5–2.5 million – Source: https://github.com/huggingface/transformers

Global Ecosystem of Users

AI/ML Engineers (1.2M – 1.8M): Full-time professionals training and deploying models using programs provided by open source Academic Users (800K – 1.2M): Researchers, grad students, and educators who also train and deploy models Indie Devs & Hobbyists (400K – 700K): Kaggle participants, open-source users, startup tinkerers Enterprise Software Devs (3M – 5M): Developers integrating AI into enterprise apps

Industry Impact

• 75%+ of Fortune 500 companies use open-source AI directly or via cloud providers • Hugging Face Hub sees millions of downloads monthly (https://huggingface.co) • GitHub’s Octoverse consistently ranks PyTorch and TensorFlow among the top OSS projects (https://octoverse.github.com/)

Top AI Companies: Builders vs. Train & Deployers

Open Source Corporate Builders: • Meta (PyTorch, Llama) • Google (TensorFlow, JAX) • Microsoft (ONNX, DeepSpeed) • NVIDIA (CUDA, cuDNN, Triton) • OpenTeams (Nebari, PyTorch, TensorFlow) Note: these companies can also train and deploy models

Open Source Train & Deploy Companies: • Amazon, Apple, Salesforce, Oracle, Palantir, Snowflake, Databricks, C3.ai, SAP, OpenAI, Anthropic, xAI Note: both Mistral and Anthropic claim to have some internal building capabilities, but as closed-box systems it cannot be confirmed

The exit constipation in the VC world stems from market regulations, not bad actors. Founders often misjudge valuation premiums offered by mega-VCs, which favor the investors. Exploring IPOs in London and Toronto can restore liquidity and allow average investors access to growth equity, improving the global economy and potentially reforming US regulations.

For those of you who are skipping to the good part (and this is the good part), you really should take a moment to go back and see how we got here (Part I, Part II).

Because there are no bad actors driving the exit constipation in the VC world, just rational economic agents doing what market deforming regulations demand. But, now that we’re here, in an exitless void, here’s how we get out of it, and save VC as an asset class in the process. This is the new path to liquidity.

When taking money from mega-VCs, GPs seduce founders with what is typically a 10%-15% premium to the market from a valuation perspective. I know this from countless discussions with the partners, principals and associates that work at these funds over many, many years. That did change between 2020-2023 during the private bubble peak, but we’ve discussed how dangerous this was for different reasons in part I and part II.

When offered a premium to the market, it is deceptively easy to take the deal and feel like you’re getting a bargain as a founder. However, founders who lack formal financial training do not realize that they are comparing a premium on common shares to the preferred shares that VCs demand. These are not the same.

As pretty much every 409(a) document attests to, these preferred shares generally command a 30% premium to common shares. In short, the 10%-15% perception of overvaluation is, in fact, a 15%-20% discount in favor of the VC.

This is why I started recommending to all our portfolio companies to begin exploring exits beyond the reach of Sarbanes-Oxley, and explore IPOs in London and Toronto. This is the new way forward.

London and Toronto have deep markets (especially deep in London) where founders can IPO after a series A or series B and get to liquidity for themselves and investors in 5-7 years, thus escaping the madness of the great VC constipation crisis. By so doing, they also make employees liquid for option pools, access better governance and oversight, as well as access to capital that can further their growth without giving up preferred share premiums.

In return, average mom and pop investors will get access to growth company stock, just like they used to prior to the whole Enron/SoX fiasco.

This is actually an important structural fix for our global economy, restoring access to higher returns to average folks, where today only the wealthy get access to companies in the growth phase through private holdings.

Exiting via London, Singapore, Toronto, Riyadh, and other viable options is not just a better economic decision, it is the moral choice for the good of humanity any way you slice it.

If more companies went public when they first became a unicorn (or even before then), then VC would go back to funding seed and series A like they used to, with some series B for good measure. There would be no market for series C because public markets have way more liquidity than Sand Hill Road could ever dream of.

Another potential outcome to fix this would be if the US Congress amended Sarbanes-Oxley so that companies with valuations less than $1bn were only subject to audit requirements, like in the old days. With a modified but lighter version for companies with market caps between $2bn and $10bn, with full SOX after that. If the US adopted this model, we’d be competitive with other countries that realized their error and fixed this mess.

Until then, I think we’ll see US equity markets continue to yield market-share to foreign markets with less liquidity, and the great VC extension will continue.

Overpriced rounds, a late stage VC bubble, and Sarbanes-Oxley are killing VC, markets and founders, as well as worsening inequality by limiting middle-class access to growth investment companies.

Overpriced rounds, a late stage VC bubble, and Sarbanes-Oxley are killing VC, investors and founders, as well as worsening inequality.

Institutional Investment in Late-Stage Venture Capital: Navigating Perverse Market and Regulatory Dynamics

Institutional investors’ sustained interest in late-stage venture capital (VC) funds is shaped by a complex interplay of behavioral, economic, and regulatory factors, despite these funds often underperforming relative to benchmarks such as the S&P 500 (see part I of this series). In this part II, I’ll examine the impacts of psychological biases, economic incentives, regulatory changes, liquidity preferences, and the evolving market dynamics that drive institutional capital toward late-stage ventures regardless of cost.

Institutional investors are often drawn to late-stage funds and the companies they back due to perceived lower risk, attributable to their established business models and proximity to liquidity events like IPOs. There is a lot of bias and false beliefs built into this system, and it has become toxic. So let’s break down what’s going on, and why allocators are funding this way.

Psychological Biases and Market Dynamics

Behavioral finance principles, such as the familiarity principle, herd behavior and the sunk-cost fallacy, are extremely relevant to investment decisions and play an outsized role in decisions to invest in late vs. early stage VC funds. Let’s cover these first.

The familiarity principle ensures that the known quantities—established companies nearing an IPO—seem safer than less predictable early-stage investments, even if they don’t provide investment returns that are positive after risk adjustment relative to the S&P 500. Because you’ve heard the names Stripe, WeWork, OpenSea, Brex, you are inclined to invest in the thing you’re familiar with, and the funds that back them. That can be a bad assumption when WeWork is the one you back.

The perceived safety of herd behavior (AKA, the bandwagon effect), wherein institutions follow the investment leads of their peers, is misleading. The assumption that the crowd knows best can also be viewed as a fear of missing out on potentially profitable opportunities. No one gets fired for following the market, so playing it safe with the pack is a reasonable strategy. Unfortunately, this is how lemmings go off cliffs.

The sunk-cost fallacy is another cognitive bias that leads many allocators to continue investing in a fund because of the time, money, or effort they have already committed, rather than cutting their losses. The rationale is often that not continuing the investment would mean that the initial resources were wasted, even though continuing does not necessarily lead to a recovery of those sunk costs.

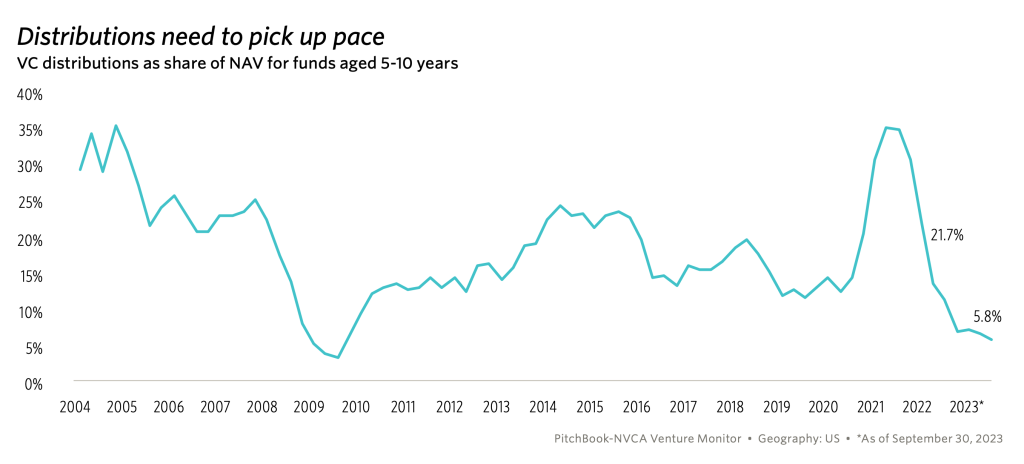

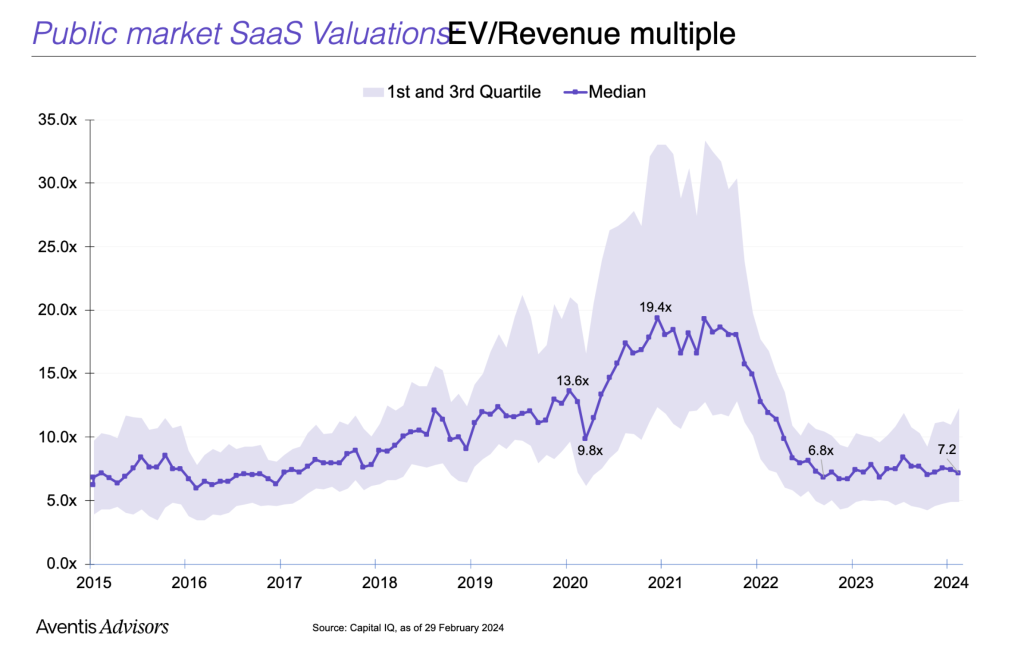

The combined effect of these three biases are beginning to be apparent when you examine flows of capital into late-stage VC funds, with LPs going along for a “ride” that seems stuck in neutral. Moreso, it may also be that allocators have lost the ability to underwrite technology, human resource, and execution risk, and are now only willing to underwrite market risk. Consider the following charts:

Distributions are at record low for a non-recessionary period, because overpriced deals over the past four years can’t be off-loaded to public markets. After pricing SaaS deals at 20x revenue just three years ago, you have a stupid amount of growth required to reach the same valuation at 7.2x revenue. Today’s valuation multiples aren’t low either, they are average for fundamental analysis based upon discounted cash flows weighted for a reasonable cost of capital in our current rate environment, unlikely to change and more realistic than the free money of the past decade.

As a result, late stage VC funds are writing larger checks to existing portfolio companies at higher and higher valuations to keep them afloat (if they’re still losing money) or in a ponzi scheme effort to keep over-marking up the winners to offset the losers. Worst of all, by delaying exits, they are not providing exit liquidity to their LPs and thus replenishing the VC funding cycle. According to JPMorgan in the Pitchbook NVCA 2023 Venture Monitor, “for vintage years 2013 to 2019, over 50% of the total value in venture funds relies on existing positions.”

Because late-stage VCs can’t IPO today without taking losses on their portfolio after writing big checks at massively inflated valuations, “unicorn” hold times increase beyond fund timelines.

What sustains this cycle is LPs willingness to keep pumping money into the late-stage funds so they can continue their sunk-cost fallacy investing on valuations not subject to public market scrutiny. Again, no one wants to recommend the “riskier” emerging manager at a small fund when the so-called experts at name brand funds are struggling to perform. Familiarity and herd bias alert!

As a result, early-stage VC is getting crowded out. The share of early-stage VC deals between $5-10mm has shrunk by 2/3. LP funds available for early-stage VCs continue to shrink. According to data from Crunchbase, 84% of capital raised by U.S. venture investors went into funds raising $250 million or more in 2018, and has increased every year since then according to Pitchbook data. As a result, VC funds managing $250m or less now account for less than half of all VC capital raised, down from over 75% in 2013. In the first two quarters of 2024, just two funds, Andresson-Horowitz and General Atlantic, raised 44% of all the venture capital raised by all VCs (Pitchbook).

While I have no data to support a hypothesis that allocators have lost the ability to underwrite technical, human resource, and execution risk, it’s clear that they are not underwriting these from the checks they’re giving VCs. Given that they only appear to be willing to invest in market risk, it seems bonkers that they do so without liquidity. You can better manage market risk in public equities with liquidity, so why do VC at all (and we’re back to part I).

This trend also shows in absolute dealmaking numbers collapsing for early-stage VC. According to AngelList, the second quarter of 2023 saw the lowest rate of early-stage startup dealmaking in the history of their dataset (dating back to 2013).

If you read part one of this series, the irony of the situation is that the VCs who continue to generate the highest returns are having the hardest trouble getting capital as late-stage VCs hoard assets and LP money. Until late-stage funds provide LPs liquidity via exits, the cash that feeds the whole ecosystem is locked up. Those exits are not likely to come soon.

Late stage VC is poisoning the well for the whole industry.

So why don’t early-stage VCs just work with founders to bypass the late-stage fiasco and encourage their portcos to go public after their series A/B rounds like we used to? Well, Congress kind of messed that up for everyone.

Impact of Regulatory Changes on IPO Timing

After the Enron scandal (which someday I’ll write a very cool post about but SoxLaw has an excellent summary here) Congress needed to show voters that they were going to do something about corporate fraud. In typical government action, they acted without fully considering the consequences of their actions. Surprise! Government is as ignorant as it is incompetent.

The resulting Sarbanes-Oxley Act of 2002 had a profound impact on the public offering landscape by dramatically increasing the cost to be a publicly traded company, imposing stricter financial reporting rules, forcing companies to hire more auditors to audit the audit (yes, that is as crazy as it sounds), and dramatically escalating governance standards for public companies.

In summary, Congress decided to stamp out fraud from corrupt auditors by adding even more auditors and creating additional byzantine governance systems for them and corrupt managers to hide in. Yes, that makes no sense.

I’ve looked at a lot of academic research to see if SOX actually reduced fraud. Without going into too much detail, it hasn’t. The best paper I can find on the topic shows that SOX only reduced the “probability” of fraud by about 1%. However, it did dramatically improve the detail of reporting provided to the public. Let’s not minimize that, and yet I’m hoping that Adam Packer will do a brilliant analysis to see if this resultes in improved investment manager performance -likely not, but surprise me!

So while SOX did dramatically improve information reporting and volume, fraud has not really decreased, valuations are down, and companies have to delay their IPOs due to increased costs and expanded public-listing responsibilities.

The average cost for SOX compliance is exploding. According to Protiviti’s annual SOX expense survey, on average, companies allocate $1–2 million for their SOX budget, with internal audit teams dedicating an additional 5,000–10,000 hours annually to SOX programs.

According to Protiviti, the average SOX compliance cost in 2023 was:

Companies with more than 10 locations: $1.6 million

Companies with only one location: $704,000

Companies with $10 billion or more in annual revenue: $1.8 million

Companies with $500 million or less in annual revenue: $651,000

When you have to shell out $1-2mm for one compliance cost, plus heaven-only-knows how many thousands of hours of additional internal audit time, you can’t go public until the economics make this massive cost immaterial.

As a result, since SOX passed, the average time from founding to IPO has notably increased—from about 5 years in the late 1990s to more than 10 years recently (Pitchbook data, thank you once again). This regulatory-induced delay significantly affects the liquidity of investments, particularly those made by early-stage venture funds, extending the time to potential returns.

So, getting liquid on VC investing is more expensive and takes longer than ever. These are the primary reasons late-stage VC is so attractive to LPs. Despite poor performance, institutional funds have a strong liquidity preference, even if the private markets aren’t beating the S&P 500 (again, see part I).

Liquidity Preferences of Institutional Investors

Given the extended timelines to IPOs, late-stage VC funds have become more attractive due to their shorter duration from investment to exit. While I can complain all day about extended unicorn hold times, the hold times are still longer if you invested earlier. Institutional investors, including pension funds and endowments, prefer investments that align with their liquidity timelines. Late-stage investments generally offer a quicker path to liquidity, matching the large pools of capital that institutional investors need to deploy efficiently.

So when average VC hold time is approaching ten years AFTER becoming a unicorn, who wants to invest in the early stage VC who backed them six to seven years before then (CB Insights, State of Venture 2023). Seventeen to twenty years is a very long time for an institutional LP to hold a private security, so who can blame them!

While I can find no solid economic research to explain why institutional investors would favor late stage VC on the basis of liquidity preferences alone, it stands to reason that a 17-year hold period is not acceptable for most funds of any size to get liquidity at any cost.

The Necessity of Large Capital Pools and the Impact on Founders

The growing average market cap of companies at IPO—from around $500 million in the early 1990s to over $2.5 billion today—requires larger rounds of late-stage funding. As companies grow larger and remain private longer, they need substantial capital to scale up to absorb the costs of a public offering post-SOX. This need makes large late-stage funds particularly appealing, as they are capable of mobilizing the capital required for continued growth. However, this trend has profound implications for startup founders, who often endure increased dilution and a loss of control as they raise more capital under increasingly stringent terms. The loss of control has real impact, as TechCrunch recently reported that VCs are using this power to block IPOs and prevent founders from liquidity. This leads to strategic misalignments that might endanger long-term success.

The assumption here by VCs justifying their control provisions is that the late-stage VC funds provide better oversight and governance and will better protect investor interests on behalf of their LPs. Really? Are VCs better and smarter than public markets and their oversight? I doubt it.

Again, I have no research (and I doubt you could put together a credible quantitative analysis), but I think it stands to reason that thousands of public investors and a public board of directors do a better job of oversight than a handful of privileged insiders who fundamentally share the same world-view as VCs. Yes, we have group-think and bias too, so better off if more eyes can see the business.

The closest thing I have to a benchmark on this is to see how company valuations change post-IPO, when public scrutiny provides the best check to the opinions of private company valuations and the ability of VCs to provide good oversight and valuation guidance. And yes, when you look at the sheer number of unicorns falling from grace since 2022, it would appear that the private markets overpriced and misgoverned significantly (see Techcrunch and Hurun).

A final note on this, if you want to nerd out on great IPO data, check out Jay Ritter’s recently updated data here. It rocks.

Diseconomies of Scale and Risks to the Ecosystem

The preference for large funds and substantial capital injections can lead to diseconomies of scale, where the size of the investments begins to detrimentally affect fund performance. As suitable investment opportunities become scarcer, funds may end up deploying capital in less optimal ventures, with more funds bidding up the price for available assets. This, in turn, can dilute returns. Moreover, as founders lose equity and control, the risk of misaligned interests increases, potentially affecting the company’s strategic decisions and long-term viability.

The larger the fund, the greater the challenge in deploying capital efficiently, which often results in decreased returns and increased risk of strategic misalignment within funded companies. Ouch.

Conclusion

Institutional investors’ preference for late-stage venture capital funding is dictated by a blend of psychological biases, regulatory impacts, liquidity preferences, the loss of their ability to underwrite anything except market risk, and the structural requirements of modern IPOs. While these investments may offer the perceived safety of shorter time horizons and reduced risk, they come with their own set of challenges, including potential misalignments and increased founder dilution.

The situation was made worse when the 2021-22 market bubble caused late-stage funds to overprice investments, and now extend exit periods so that they can avoid going public at a loss. Without exits, no new liquidity is flowing back into institutional and large family office LP investors, so early-stage VC funds are getting squeezed with fundraising for new funds that have ever elongating exit strategies. This, in-turn, creates less companies getting funded to their series A/B, and further restricting deal flow for late-stage funds, thus exacerbating their crisis to allocate capital and double down on their already overpriced, current portfolio companies.

So how do we break this doom-cycle? Part III coming soon…

Late stage VC funds are earning dismal returns relative to the S&P 500 and take little risk. So why are LPs continuing to fund them? What the heck is happening in VC and can we fix it?

Welcome to the world of unlevered, illiquid, venture investing!

In this bizarro world, bigger is worse, and investors don’t seem to care.

What is going on?

Part One of a Three Part Series

Venture Capital Returns by Fund Size: Comparing Early-Stage vs. Later-Stage

Venture capital (VC) is a critical component of the financial landscape, fueling innovation and growth within the startup ecosystem. However, the returns on venture capital investments can vary significantly based on several factors, including the stage of investment and the size of the fund. Without trying to boil the ocean, I’m going to do a quick look at how venture capital returns diverge by fund size, with a specific focus on comparing early-stage and later-stage VC investments. Additionally, I want to cover how early-stage funds, particularly those smaller than $250 million, often outperform their larger counterparts, especially when compared against broader market benchmarks like the S&P 500.

Venture capital funds are typically classified into different stages based on the maturity and revenue of the companies they invest in: early-stage (Seed and Series A), mid-stage (Series B and C), and later-stage (pre-IPO financing). The size of these funds can also vary, ranging from small funds (less than $250 million) to large funds (more than $1 billion).

Later-Stage VC: Higher Risk with Lower Relative Returns Relative to Early Stage VC

Later-stage venture investments involve funding more established companies that are closer to a public offering or a major liquidity event. These investments are perceived as less risky compared to early-stage investments because the companies have proven business models and steady revenue streams. However, the return on later-stage investments can be less attractive compared to early-stage investments on a risk-adjusted basis. According to data from Cambridge Associates, later-stage VC funds have demonstrated lower returns compared to early-stage funds. The 10-year pooled return for later-stage funds as of 2020 was around 12%, significantly lower than the returns generated from early-stage funds which averaged around 20% (1). I’m looking for more recent data, because I’d bet my bacon that late stage fund returns went down, a lot, on average. At least, that’s what institutional LPs tell me, a lot. So much so, I wonder why they keep investing (that is part II of this essay).

Moreover, when comparing these returns to the S&P 500, which delivered a historical average annual return of approximately 8% to 10% with considerable liquidity, the attractiveness of later-stage VC diminishes further. The lack of liquidity and higher relative risk associated with late-stage venture investments, combined with returns that do not commensurately reward this increased risk profile, makes them less appealing compared to other investment opportunities. And yet, late stage VC keeps on raising money, lots and lots of money.

Early-stage venture capital involves investing in startups at their nascent stages, typically while their revenues are $3mm a year or less. These investments are inherently riskier due to the unproven nature of the businesses and their higher likelihood of failure. However, the potential for high returns is significant, especially for top-performing funds. A pivotal study by Cambridge Associates shows that top decile early-stage venture capital funds, particularly those with under $250 million in assets, have significantly outperformed their larger counterparts and broader market indices. The top decile of early-stage funds reported returns as high as 35%, showcasing exceptional performance that should attract sophisticated investors (2).

This performance variance can be attributed to several factors. Smaller early-stage funds are often more agile, able to make quick decisions, and invest in innovative startups that larger funds might overlook. Additionally, these smaller funds can provide more hands-on support to their portfolio companies, contributing to their chances of success.

That’s where early-stage VCs can generate massive alpha, and late stage simply can not because the companies are already significantly de-risked. Risk equals reward, and those who manage risk better, can earn returns in excess of their risk adjusted expectation. Later stage VCs require less risk-management ability, and their relatively poor returns reflect this.

Comparative Analysis with the S&P 500

When compared to the S&P 500, top-performing early-stage venture capital funds offer much higher returns, albeit with greater volatility and liquidity risk. For investors, this trade-off is often acceptable due to the substantial premiums involved. According to the National Venture Capital Association, early-stage funds not only surpass the S&P 500 in terms of returns but also contribute significantly to job creation and technological advancements, thereby offering both financial and societal benefits (3).

Part II Teaser

In summary, while venture capital as an asset class can offer high returns, the variability of these returns based on the stage of investment and the size of the fund is significant. Later-stage venture capital, despite its lower risk profile relative to early-stage investments, often fails to provide returns that justify the risks and illiquidity involved. Conversely, smaller early-stage funds, particularly those making Seed and Series A investments, consistently outperform not only their later-stage counterparts but also the broader market indices like the S&P 500 when considering top decile performers. These findings underscore the importance of strategic fund selection based on detailed performance data and fund characteristics in the venture capital industry.

So how did we get here? Why are LPs piling into bigger and bigger funds that offer returns lower, and lower each year? This makes even less sense when we consider that the S&P has been recently beating late stage VC returns, WITH LIQUIDITY!!!

【1】Cambridge Associates, US Venture Capital Index and Selected Benchmark Statistics 【2】Cambridge Associates, US Venture Capital Index 【3】National Venture Capital Association, 2020 Yearbook

We have to humbly face the truth that as a founder, you are probably making something you love. Make something other people love if you want to succeed.

Make Products People Love – Part One

This is the first part of a three part series on how founders can make products people love. To begin, we have to humbly face the truth that as a founder, you are probably making something you love. Make something other people love if you want to succeed.

Unlearning is a transformative process that involves the deliberate effort to change or discard previously acquired knowledge, beliefs, or behaviors that are found to be incorrect, outdated, or harmful. When you want to make something other people will love, the ability to unlearn things you may love becomes crucial in avoiding customer ignorance and fostering a culture of continuous learning and growth in your startup. This post explores the significance of unlearning when making something people love, outlines strategies to facilitate unlearning for yourself and your company, and examines the challenges and benefits of this process to finding product-market fit.

Understanding Ignorance and the Need for Unlearning

Ignorance, in this context, refers to a lack of knowledge, understanding, or awareness about a customer or the broader complexities of your customer’s needs and values. It can stem from outdated information, misconceptions, biases, or the inability to access or interpret new information accurately. Ignorance most often is not the absence of knowledge but holding onto incorrect or incomplete information as truth.

Unlearning addresses this aspect of ignorance by challenging our current knowledge base and making room for new, more accurate information. It is a deliberate process that requires recognizing that some of what we know may be wrong or incomplete and being open to changing those understandings. Unlearning is essential in a world where technological advances, societal shifts, and new scientific discoveries constantly reshape our understanding of reality, and our customer’s needs and preferences constantly change with it.

Strategies for Unlearning

Reflective Practice: Engage in regular reflection on your beliefs, knowledge, and behaviors in regard to who your customer is, what they value, and how they use the product. Question the origins of your assumptions and the evidence supporting them. Reflective practice encourages a critical examination of one’s understanding and opens the door to recognizing areas in need of unlearning.

Seek Out Diverse Perspectives: Exposing oneself to different customer viewpoints and experiences is vital in challenging customer ignorance and fostering new learning. This exposure can highlight gaps in knowledge or biases, providing opportunities for unlearning and relearning. We STRONGLY encourage our founders to conduct hundreds of customer interviews using methodology outlined in the Mom Test to accomplish this.

Embrace Vulnerability and Curiosity: Admitting that one’s knowledge may be flawed or incomplete requires vulnerability. Approaching learning with curiosity rather than defensiveness allows for a more open and effective unlearning process. Take joy when you realize you’re wrong about something.

Critical Thinking and Media Literacy: Develop skills in critical thinking and media literacy to better evaluate the accuracy and bias of the information being consumed. This skill set is crucial in distinguishing between credible information and misinformation or outdated knowledge.

Continuous Learning: Commit to lifelong learning as a mindset. Recognize that knowledge is ever-evolving and that staying informed requires ongoing effort to learn, unlearn, and relearn. Nelson Mandela once said, “I never lose. I either win or learn.” When you’re always learning, you’re always winning!

Challenges in Unlearning

Unlearning is not without its challenges. Cognitive biases, such as confirmation bias, can hinder our ability to see beyond our current beliefs and accept new information. Emotional attachments to certain beliefs or the discomfort of cognitive dissonance can also make unlearning difficult. Additionally, team, social and cultural pressures can reinforce outdated or incorrect beliefs, making the process of unlearning even more challenging for product development. Pivoting or abandoning beloved features when they don’t offer value can be painful if we’re emotionally and socially committed to them.

You and your team are preprogrammed to like things that reinforce your feelings and ideas, just one of many biases you should be familiar with. The Decision Lab has an amazing list of cognitive biases that is worth your time to study. The more bias you recognize, the better you can figure out your Dunning-Kruger reality, so to speak (click the bias link if you’re curious about Dunning-Kruger, no worries if you already know it all, wink, wink).

The Benefits of Unlearning

Despite these challenges, the benefits of unlearning are profound. First, it fosters a more accurate understanding of your customer, enhancing your ability to make informed product decisions based upon their needs and willingness to pay. Second, it promotes flexibility and adaptability, qualities essential for a start-up to find product-market fit. Third, unlearning can lead to personal growth and improved relationships, as it encourages empathy and understanding by challenging our biases and assumptions about others. This means that the team that unlearns the best, is the team that also works together most efficiently. Win-Win!

Final Thoughts

In a world saturated with information and where knowledge is continuously evolving, the ability to unlearn is as crucial as the ability to learn when doing customer research. Unlearning allows us to shed outdated, incorrect, or harmful beliefs and behaviors about our customers and ourselves, making room for new information and perspectives that foster trust and understanding. You will, in turn, build something people love because you know them. This process is essential in avoiding ignorance and fostering a culture of continuous growth and improvement.

While unlearning presents challenges, particularly in overcoming cognitive biases and emotional attachments, the benefits it offers are substantial. By adopting strategies such as reflective practice, seeking diverse perspectives, embracing vulnerability, and committing to continuous learning, start-ups can navigate the complexities of unlearning, identify the true customer need, and make something people want. Ultimately, unlearning is not just about discarding old knowledge but about making space for new understandings that lead to product success.

Over the past year, many ESG (Environmental and Social Good) focused funds have reported dismal returns and are either shutting down, or dramatically lowering expectations for performance with their LPs and hoping for mercy. And yet, with our fund I, performing remarkably well, we have INSANE ESG impact without looking for it per se.

However, upon closer inspection I realized that our massive consumer surplus definition of a good investment embeds within it an Easter egg that can not be uncoupled from consumer surplus: environmental and social good.

Consumer surplus is a economic foundation that most VCs ignore, but I cover exhaustively. It is the difference between what you’re willing to pay, and actually pay. Great stuff that can be adopted faster will always dramatically improve consumer surplus. Embedded within this economic truth is an ESG reality: services and technology that massively improve consumer surplus not only improve economic outcomes, they improve social and environmental ones by default.

If consumer surplus goes up, ESG impact must by definition increase. Consider these two examples from our portfolio.

1: Fila Manila is now the #1 Filipino food leader in the US. When we invested in the company, the space was pretty empty. If you wanted Filipino food in the US, you had to either go out to eat at one of the hard-to-find restaurants that served it, or spend hours in the kitchen preparing it. When you buy it in the store, you save time, gasoline, effort, etc. There is an environmental and economic benefit. Socially, we benefit from an expanded culinary palette with greater awareness of the rich culture and beauty of the Philippines.

2: Nitex is quickly becoming the largest supply chain management system for the global fashion economy. By implementing this software, fashion companies save millions of dollars by dramatically reducing travel to manufacturing sites, often in hard-to-reach developing economies around the world. They also can respond faster to changes in demand, dramatically reducing overproduction in an industry responsible for most industrial water use and contamination. In short, Nitex is not only a good choice economically, massively driving down supply chain costs, but cuts out an insane amount of carbon from air travel and dramatically reduces the need to over consume precious water resources.

As we look across our portfolio, we see that when selecting companies based upon strict consumer surplus benefit criteria, our process bakes in an automatic ESG component because improved economics ALWAYS improves ESG if you measure value by this metric. By flipping ESG selection around, looking for incredible consumer surplus impact first, we’re hard-coding our fund to only invest in ESG positive companies because they secretly go hand-in-hand.

Perhaps ESG funds should consider doing the same? Focus on game-changing, consumer-surplus generating ideas, and reap the ESG benefits that naturally occur when you invest for impact with strict economic benefits in mind.

To do ESG right, let consumer surplus be your guide. Economics align with environment and social good when we invest wisely.

A final note: new, exploitive technologies do not generate consumer surplus, they profit from monopolies or exogenous factors such as chemical addiction and resource exploitation for short-term financial gains and massive negative externalities born by someone else. Again, consumer surplus leads the way in accounting for and avoiding such schemes.

We’ll venture through four stages: Awareness, Consideration, Decision, and Loyalty / Advocacy and examine how to save customers from fire swamps that slow them down along the way.

Whether you’re just starting to sell or you’re deep in the weeds of growth marketing, understanding your customer’s journey from awareness to rabid fandom is essential. Founders, let’s map your customer’s epic quest inspired by the timeless classic, The Princess Bride. We’ll venture through four stages: Awareness, Consideration, Decision, and Loyalty / Advocacy and examine how to save customers from fire swamps that slow them down along the way.

Scaling the Cliffs of Awareness

To get to happily ever after, customers must first scale the Cliffs of Awareness. So, how do you make your potential customers aware of your offering?

Riddle me this:

I am what you seek to spread the word, A means to make your product heard. To solve the puzzle, it’s plain to see, Experimentation is the key.

Hint hint: there are 19 different channels that can be employed to build awareness, but only 1-2 will help your customers find you. The only way to find these channels is to test. Examples of these channels include:

Once you identify your top performing channel, monitor its performance (e.g., how many clicks did your ad campaign get?) and test different messaging. Guide your customers, like Fezzik carrying his companions up the rocky cliffs, safely to your offering.

Wading Through the Fire Swamp of Consideration

After your customers ascend the Cliffs of Awareness, they face a deluge of choices, like Westley and Buttercup navigating the perilous Fire Swamp.

As they research and evaluate their options, aid them in their quest by following these steps:

Understand their priorities. (e.g., choosing between Apple iPhone and the Samsung Galaxy, the customer might consider price, features, design, and/or brand reputation)

Create buyer-centric content: Develop content that addresses your audience’s specific needs at each stage of the buyer’s journey. (e.g., Zillow’s comprehensive home buying guides.)

Leverage lead nurturing: Use email marketing, retargeting ads, and personalized content to keep leads engaged and guide them towards a decision. (e.g., Everlane’s targeted promotions.)

Empathize with your customer’s pain points and fears, and create content and testimonials that showcase your brand’s unique qualities. (e.g., Airbnb’s user-generated reviews and experiences.)

Are customers getting past the Cliffs of Awareness but struggling to make it past the Fire Swamp of Consideration? The only way to know is to measure and test messaging! (e.g., how many people clicked on your retargeting ads)

The Pit of Purchase Decisions

In the decision stage, customers have chosen a solution and are ready to buy. If your purchasing process is as torturous as the Pit of Despair, your customers will go no further and peril.

If your customers are emerging victorious from the Fire Swamp of Consideration but dropping off in the Pit of Purchase Decisions (e.g., abandoned cart), attempt to save them just as Miracle Max saved Westley when he was “mostly dead”. Here are some tricks to try:

Count the clicks: Know how many actions it takes for the customer to buy and make it as easy as humanly possible (e.g., Amazon’s one-click purchase; guest checkout; credit card autofill and Apple Pay)

Email your customers to bring them back to their abandoned purchase. You can even deploy product promotions (e.g., “Sign up now and save 30%”) to sweeten the deal.

Re-examine your demo or sales script. Have an experienced sales person sit in on a closing call or review emails sent in the closing process, implement the feedback and test the new messaging.

Happily Ever After: Loyalty and Advocacy

Congratulations, you’ve won the battle, but the journey is far from over. You don’t want a fake, short relationship (Boo!) like that of the King and Princess. Create a true and everlasting love between your customers and company like that of Westley and Princess Buttercup.

Here are some strategies to foster loyalty:

Exceed customer expectations: Go above and beyond to deliver a memorable experience that surpasses their expectations. (e.g., Chewy delivers flowers when a pet passes away and has an exceptional return policy)

Personalize customer interactions: Use data insights to tailor your marketing efforts, offers, and communications, creating a bespoke experience for each customer. (e.g., Spotify Wrapped)

Implement a loyalty program: Reward loyal customers with incentives such as discounts, exclusive offers, or early access to new products. (e.g., Starbucks Rewards program.)

Regularly request feedback: Actively seek customer feedback and demonstrate your commitment to improving their experience by implementing frequently mentioned suggestions.

When you show your customers love, advocacy becomes more natural.

However, if customers need a nudge to shout their love from rooftops, here’s a trick:

As we close the storybook on our Princess Bride-inspired customer journey, remember the lessons learned from Westley, Buttercup, and their friends. From the rocky Cliffs of Awareness to the triumphant Happily Ever After, this quest is yours to write. And when you help your customers every step of the way, they will live another day to pass along the story of the great quest. After all, the best person to help a new customer up the Cliffs of Awareness is a friend who has emerged triumphant.

Shariah compliant VC funds provide proven economic benefits to LPs, GPs and portfolio companies including higher rates of return, diversity, less volatility in portfolio returns, and better alignment with environmental and social good.

Last fall, Oksana and I met with hundreds of prospective Limited Partners for our new fund. Among those who we realized had the best fit, were a significant number of Muslim investors, and they had some great ideas about how we could improve our fund performance by becoming a Shariah compliant fund.

Investing in Shariah compliant funds has gained popularity in recent years, as investors seek to align their investments with their values and beliefs. Shariah compliant funds follow Islamic principles (but are not limited to Islamic investors) and avoid investments in sectors such as alcohol, tobacco, gambling, and pornography.

Given our unadulterated devotion to ethically improving returns for LPs, we did our research and discovered that Shariah compliance is a fast growing investment market and provides many proven economic benefits to LPs, GPs and portfolio companies, including: higher rates of return, diversity, less volatility in portfolio returns, and better alignment with environmental and social good.

According to a report by the State of the Global Islamic Economy (SGIE) in 2020, the assets under management (AUM) of Shariah compliant funds had grown from $58 billion in 2009 to $121 billion in 2019, representing a compound annual growth rate (CAGR) of 6.7%. The report also projected that the global AUM of Shariah compliant funds would reach $174 billion by 2023. This is pretty impressive when you consider that CAGR is almost double traditional fund inflows.

On the economic benefits, the first advantage of investing in Shariah compliant VC funds is that they offer the potential for higher returns than traditional VC funds. A study by the Islamic Development Bank in 2015 found that the average annual return of Shariah compliant VC funds was 16%, compared to 13% for non-Shariah compliant VC funds. The study also found that Shariah compliant VC funds had a higher success rate in exiting their investments, with 78% of their investments successfully exiting, compared to 62% for non-Shariah compliant VC funds.

Secondly, Shariah compliant VC funds offer investors a way to diversify their portfolios. These funds typically invest in startups that are aligned with Islamic principles, which means they are likely to invest in a range of sectors such as healthcare, technology, and renewable energy. A study by the University of Maryland in 2015 found that Shariah compliant funds were more diversified than non-Shariah compliant funds, which reduced the overall risk of the portfolio. This means that investors can benefit from the potential for high returns from investing in startups, while also reducing the risk of their overall portfolio by diversifying.

Diversity leads to less volatility, our third area of economic benefits. In a study by Khediri and Charfeddine (2016) found that Shariah compliant funds exhibit lower volatility due to the diversification of their portfolios. The study analyzed the performance of Shariah compliant and conventional mutual funds in the Gulf Cooperation Council (GCC) countries and found that Shariah compliant funds had lower levels of volatility. The authors attributed this to the diversified nature of Shariah compliant funds.

Shariah fund reduced volatility is not only from their diversity, but is hard-wired into their selection process. According to a study by El-Gamal et al. (2017) found that the screening process used by Shariah compliant funds tends to exclude companies that are highly leveraged, which can reduce the risk of investment losses in volatile market conditions. The authors also noted that Shariah compliant funds tend to focus on long-term investments, which can lead to a more stable investment portfolio. Holy alpha!

Fourth, investing in Shariah compliant VC funds can provide investors with a way to make socially responsible investments. Shariah compliant funds avoid investing in sectors that are deemed harmful to society or the environment, such as alcohol and tobacco. This means that investors can align their investments with their values and beliefs, while also potentially generating higher returns. A study by the Harvard Business Review in 2017 found that companies that focus on social and environmental issues tend to outperform those that do not, which suggests that investing in socially responsible startups can lead to higher returns.

And as a secret bonus, Shariah compliant VC funds offer investors access to investment opportunities that are not available through traditional VC funds. These funds tend to invest in startups that are based in emerging markets, such as Asia and the Middle East, which have high growth potential but may be overlooked by traditional VC funds. A study by the University of Cambridge in 2017 found that Islamic finance institutions were more likely to invest in small and medium-sized enterprises (SMEs) than conventional finance institutions, which suggests that Shariah compliant VC funds may be more likely to invest in startups that are in the early stages of development and have higher growth potential to late-stage VC funds.

So yeah, we went all-in for Sharia compliance with zero regrets! Yeah, we want to generate higher returns with greater diversification, less volatility, invest in a sustainable and socially responsible manner, provide access to unique investment opportunities, and crush benchmarks for top decile funds. While there is no guarantee of returns with any investment, the academic research and published studies suggest that investing in Shariah compliant VC funds can be a viable option to make all our GP dreams come true.

If you’d like to learn more about Shariah compliance and VC investing, here’s links to the articles we mentioned above, and a few more we found interesting. Enjoy!

Polite people don’t want to tell you, “your baby is ugly.”

Many early stage entrepreneurs are truly baffled by the fact they get wonderful feedback from prospective clients, and may even have some unpaid pilots, but when asked to buy, customer silence is soul-crushing. Said one founder, “literally, everyone I show this to tells me what I’m building is awesome and they love it, but then I ask them to buy it and they go dark.”

If this is you, I’m about to reveal a shocking truth: they’re lying to you.

Polite people don’t want to tell you, “your baby is ugly.” So, humans tell white lies and say, “that is amazing.” Amazing, awesome, great, and beautiful are perfect words. They, and their many friends, convey a sense of wonder and accomplishment that doesn’t convey the fact that the person has zero need for what you’ve built.

If you want to get past platitudes, stop showing people your product and start asking them smart questions:

How do you currently solve this problem?

Why do you do it this way?

Would you change anything about this?

How would changing that help you?

Will you walk me through how that happened last time?

Who pays for this and why?

Is there anything else I should be asking to understand this better?

May I observe how you work to understand what you do better?

Who else should I be talking to to learn about this?

If you have a cunning grasp for the obvious, you’ll notice that none of these questions are about your product/service or introducing it in any way. That is precisely the point. If you want to sell something, stop selling and start listening.

Studies show that if you allow your customer to talk around 60% of the time on a call, you have the highest probability of success. I generally recommend an 80-20 ratio, since I find most people don’t realize how much they are talking (myself included), and by targeting 20%, they end up closer to 40%.

When you ask questions about how a customer solves a problem and why they do it, you’ll gain insight on their interest and develop a better solution. Don’t worry, they’ll get to your solution soon enough. Focus on them first, and the sales will follow.