Current AI economic and technological assumptions are about to change dramatically. As Nebari enables everyone to have their own intelligence hub, we have to re-think AI.

A Strategic Framework for World Leaders

By Joe Merrill

Artificial intelligence is entering its infrastructure phase. Today’s global market favors large foundation models, hyperscale data centers, and centralized compute. That preference is rational given current benchmarks and capital flows.

However, it is incomplete.

The next phase of AI competition will not be determined solely by model size. It will be determined by ease of use, orchestration, energy efficiency, and control of inference across distributed systems for higher fidelity at global scale.

Large models will remain essential. But they will not remain dominant for every task. Nations and enterprises that assume scale alone guarantees superiority risk overinvesting in centralized infrastructure while underinvesting in distributed intelligence that is easy to use.

This outline does not argue against frontier models. It argues that frontier models are not the final architecture.

I. The Current Market Logic

The present AI economy rests on three defensible assumptions:

Centralization simplifies governance and security.

These assumptions are supported by scaling laws and benchmark performance. Frontier models demonstrate remarkable cross-domain capability.

But general capability is not the same as economic optimality and high fidelity.

Most enterprise and governmental AI use cases are bounded:

Fraud detection

Logistics optimization

Energy forecasting

Compliance automation

Defense modeling

These tasks require precision within domain constraints. They do not require universal reasoning engines.

The central question is no longer:

Who can train the largest model?

It is:

Who can deliver optimal inference at sustainable cost and sovereign control?

II. The Immutable Law of Tensor Data

The Immutable Law of Tensor Data: For any AI inference problem, there exists an optimal quantity and structure of information required for accurate tensor inference. Data beyond this threshold introduces inefficiency, noise, or spurious correlation.

This is not a rejection of scaling laws. It is a refinement of them.

Scaling improves generalization when the task is unknown. But when the task is known, excess context can:

Increase energy consumption

Introduce irrelevant correlations

Reduce interpretability

Increase attack surface

Inflate cost

The future advantage belongs to those who know:

What information is necessary

What information is irrelevant

How to structure data for optimal tensor efficiency

The race is not for the largest model. It is for the most efficient, high-fidelity signal.

III. The Role of Large Models in Future Architecture

Large models will remain critical for:

Frontier reasoning

Multimodal synthesis

Model distillation

Bootstrapping domain systems

They are analogous to supercomputers in the 1980s. Essential. Specialized. Powerful.

But they will not be the operating layer of global AI.

Over time, most production workloads will shift toward:

Smaller domain-optimized models

Routed model architectures

Edge inference systems

Hybrid compute clusters

The winners will orchestrate across model sizes, not bet exclusively on one.

IV. Lessons from Distributed Computing

In the late twentieth century:

Supercomputers built by Cray remained essential.

But distributed personal computing, enabled by Microsoft and Intel, reshaped the global economy.

Centralized compute did not disappear. It became one tier in a layered system.

The transformative shift came from:

Standardized operating layers

Modular hardware ecosystems

Distributed deployment

Lower barriers to participation

AI is approaching a similar inflection.

V. The Strategic Vulnerability of Hyperscale-Only Thinking

Hyperscale infrastructure carries real strengths:

Economies of scale

Rapid iteration cycles

High hardware utilization

But it also introduces structural risks:

Energy concentration

Supply chain dependence

Geopolitical leverage imbalances

Latency bottlenecks

Data sovereignty conflicts

Single point of failure security

Centralization optimizes for providers. Distributed orchestration optimizes for users and nations.

Resilience, cost and fidelity increasingly matters more than scale prestige.

VI. Orchestration as the Decisive Layer

The core strategic question is not large versus small models.

It is:

Who controls orchestration across heterogeneous models and distributed compute?

OpenTeams’ Nebari provides:

Model lifecycle management

Multi-model routing

Sovereign deployment environments

Distributed compute orchestration

Integration across public, private, and edge systems

Nebari does not replace frontier models. It integrates them.

Just as operating systems abstracted hardware complexity, AI operating layers will abstract model heterogeneity.

The dominant power in the AI era will not be the largest model builder. It will be the orchestrator of inference.

VII. Addressing Common Objections

“Frontier models outperform small models.”

True in general benchmarks. False in most bounded enterprise contexts, research, and science.

Performance must be measured relative to task constraints and cost.

“Distributed systems are more complex.”

Without orchestration, yes. With standardized orchestration, no.

Complexity migrates from the user to the platform.

“Hyperscalers can integrate orchestration themselves.”

They will attempt to.

But sovereign environments require:

Cross-cloud interoperability

On-premise integration

Air-gapped deployments

National control layers

No single hyperscaler can credibly serve every sovereign boundary without conflicts of interest.

The opportunity lies in neutral orchestration.

“Capital markets favor hyperscale.”

Markets often overconcentrate in infrastructure cycles. Telecommunications, railroads, and fiber optics all experienced this pattern.

Distributed optimization historically follows central buildout.

VIII. Implications for Data Centers

Data centers will not disappear.

They will evolve toward:

Regional clusters

Energy-proportional scaling

Edge compute augmentation

Hybrid public-private orchestration

Instead of monolithic GPU concentration, we will see federated compute networks.

Energy economics will drive this transition.

IX. Strategic Guidance for Nations

World leaders should pursue dual-track strategies:

Maintain access to frontier model capability.

Invest aggressively in distributed orchestration and domain models.

True sovereignty does not mean replicating hyperscalers.

It means controlling inference pathways, data governance, and energy exposure.

X. Conclusion

The current AI paradigm is not wrong. It is incomplete.

Large models expand possibility. Distributed orchestration secures sustainability. Small models are the path to efficient fidelity.

The Immutable Law of Tensor Data reminds us:

Intelligence is not maximized by volume alone. It is maximized by relevance and structure.

The coming era will reward those who:

Optimize signal over scale

Distribute rather than concentrate

Orchestrate rather than centralize

Build resilience rather than prestige

History does not eliminate centralized systems. It absorbs them into distributed architectures.

When AI makes public decisions, the public must understand how. National defense and public infrastructure demand government owned, open source AI.

Sovereignty First If governments don’t control their own AI, AI contractors will control the government. National defense and public infrastructure demand government owned, open source AI.

Transparency or Tyranny Closed AI hides bias and evades accountability. Open source lets us audit, improve, and trust the systems that govern our lives.

Stop Renting Intelligence Proprietary AI binds the government into expensive, locked vendor contracts. Sovereign AI builds national strength and saves taxpayer dollars.

Build Once, Share Often Open systems allow agencies to integrate, innovate, and collaborate, without starting from scratch or compromising national security.

AI Must Serve the People When AI makes public decisions, the public must understand how. Open source ensures oversight and public trust.

The U.S. has an opportunity to lead the world in AI, but only if we make the right choices now. The federal government must mandate open-source AI adoption across defense, intelligence, and public services, ensuring that the code that runs our country belongs to the people, not private corporations.

If the government doesn’t control its AI, then the AI will control the government

By Joe Merrill, CEO, OpenTeams

Artificial intelligence is reshaping national security, defense, and public infrastructure at a breathtaking pace. Governments around the world are deploying AI to modernize operations, improve intelligence capabilities, and optimize decision-making. But there’s a fundamental question that the U.S. must answer now: Who should control the AI that powers our government?

The recent White House call for an AI Action Plan under Executive Order 14179, Removing Barriers to American Leadership in Artificial Intelligence (January 23, 2025) calls for a united commitment to removing regulatory obstacles, fostering private sector innovation, and maintaining U.S. global leadership in AI. However, we believe one fundamental principle must guide AI adoption in government: the U.S. must own, control, and understand the AI that powers our national infrastructure.

This means prioritizing open source AI, where the code is transparent, auditable, and government controlled over proprietary, black box systems managed by private companies with competing interests and opaque security risks.

We’ve already seen how relying on black box AI systems can backfire:

The Pentagon’s JEDI Cloud Failure – The Department of Defense originally awarded a $10 billion contract for a proprietary AI powered cloud system. But after years of delays, lawsuits, and concerns about vendor lock-in, the project was scrapped in favor of a multi-vendor approach that embraced open architectures.

The VA’s AI Powered Scheduling Debacle – The Department of Veterans Affairs attempted to modernize patient scheduling using proprietary AI software. The result? Technical failures, mismanagement, and a $2.5 billion project collapse that left veterans waiting longer than ever.

Police Departments and AI Bias – Cities across the U.S. have adopted closed AI facial recognition tools that have been shown to misidentify minorities at alarming rates. Without open access to the algorithms, the government has little ability to audit, correct, or improve these systems.

The European Union has begun passing laws banning government use of black-box AI in critical applications, recognizing that if the government doesn’t control its AI, then AI controls the government. The U.S. must follow suit.

Here’s five reasons why America needs to wake up immediately and fix this urgently:

National Security & Sovereignty – AI should be controlled by the U.S. government, not private companies with financial interests or foreign ties. Open source AI ensures that we own and understand the technology that powers our defense, intelligence, and critical infrastructure.

Transparency & Accountability – Unlike proprietary AI, open source models allow the public and independent experts to audit decisions, reduce bias, and prevent hidden agendas.

Cost Efficiency – The government shouldn’t pay licensing fees to private AI vendors indefinitely. Open source AI eliminates vendor lock-in, reducing costs over time and allowing the government to invest in internal AI expertise.

Interoperability & Innovation – Open systems integrate with existing technology and foster innovation by allowing agencies to build on top of each other’s work rather than reinventing the wheel.

Public Trust – When AI makes decisions that affect millions of Americans, from loan approvals to prison sentencing, citizens deserve to know how those decisions are made. Open source AI enables transparency and accountability.

The U.S. has an opportunity to lead the world in AI, but only if we make the right choices now. The federal government must mandate open source AI adoption across defense, intelligence, and public services, ensuring that the code that runs our country belongs to the people, not private corporations.

As the White House moves forward with its AI Action Plan, open source AI must be a central pillar of America’s strategy. National security, economic independence, and democratic accountability depend on it.

The future of AI should be open. Let’s make it happen.

AI training and deploying companies are trying to capture your data. An understanding of the industry economics can help you avoid this pitfall.

Artificial Intelligence (AI) is often framed as the domain of a few elite companies. But a closer look reveals a massive gap between those who actually build AI and those who put wrappers on it, train it, and resell it.

The actual numbers for who builds AI are shockingly small. Only a small number of companies, primarily five, contribute to open-source AI at scale: Meta, Google, Nvidia, Microsoft, and OpenTeams. In saying so, I also want to point out smaller and significant contributions from companies like Stability AI, EleutherAI, and Mistral, who all make meaningful code updates and changes despite their smaller size.

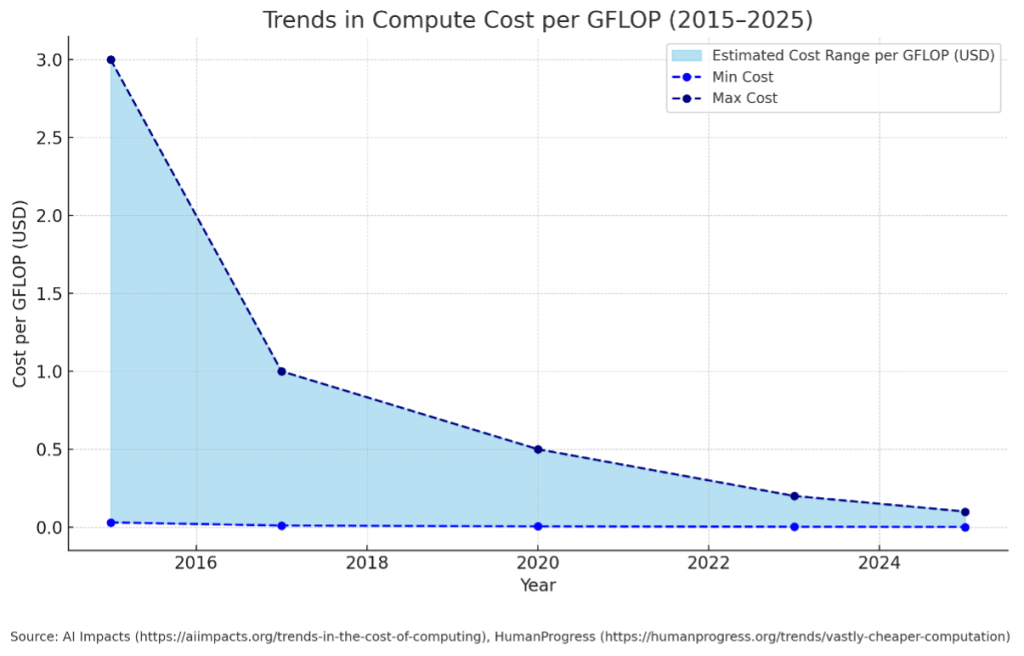

Because open source AI is free to download doesn’t mean it is free to operate. Like adopting a puppy, you still have non-trivial startup costs and maintenance. However, these expenses are not what industry developers have traditionally suggested and are shockingly affordable for most enterprises.

These economic factors combine to produce an AI industry with barriers ironically related to human development and not compute. Just as the best time to plant a tree is 20 years ago, the best time to create new AI developers was a long time ago. It will take a generation to produce adequate supply for the field due to lengthy training requiring PhD level know-how in mathematics, statistics, and computer science plus years of coding experience.

On the technical input side of the AI building equation, training costs are collapsing and with an increasingly high-quality library of pre-trained, open source models already available, everyone can have their own AI. Indeed, those who don’t will be at the mercy of those who do.

Shareholders and voters will not buy the story that giving away their competitive and personal data to AI oligarchs is economically necessary or valuable. Communal LLMs are economically inefficient, epistemically noisy, and strategically reckless for any enterprise or government that values performance, accuracy, or control of its intellectual property. The privacy risks inherent in communal models are real. The future of AI will be enterprises owning their open source AI to save costs, provide accurate answers, and protect their intellectual property. This is the efficient market solution preferred to communal LLMs sucking massive power to untangle spurious correlations from superfluous data.

To be sure, black-box AI SaaS providers will still have a business model as “drivers” of AI as opposed to those who build and deploy it. However, that economic pie will be smaller just as F1 drivers still do financially well, but nowhere near the economic returns earned by those who build cars. The upstream builders of AI will always have an advantage when deploying and training models because of the advanced know-how they possess to optimize AI and fully take advantage of its capabilities.

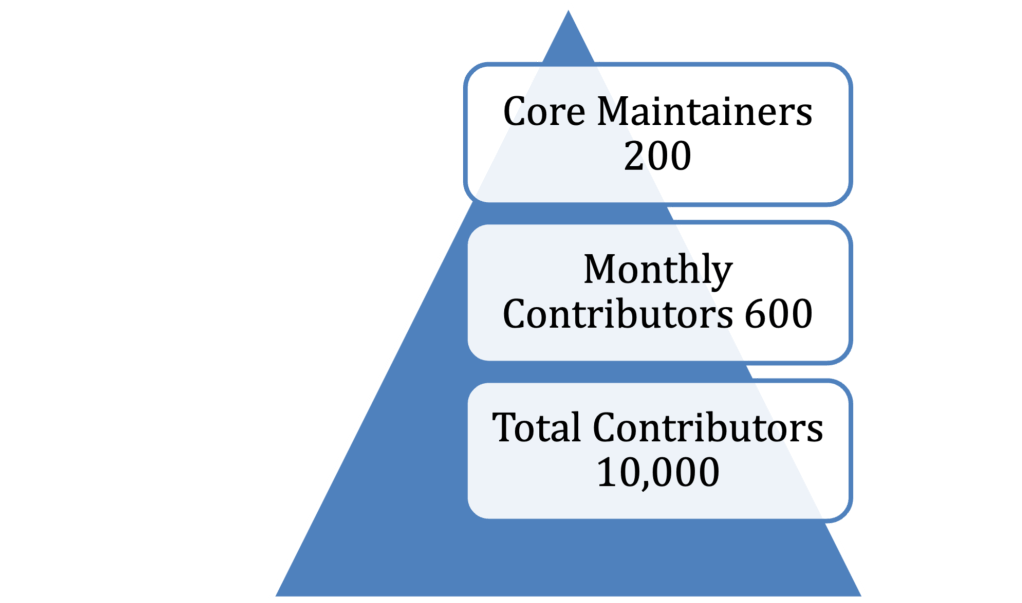

The AI Industry Pyramid

Below is a visual representation of the AI workforce, from elite maintainers to the broader ecosystem of users:

Detailed Platform Stats

1. PyTorch – GitHub contributors: ~3,900+ – Monthly active contributors: ~250 – Core Maintainers: 80 – Users: ~4–5 million – Lead Developer: Meta AI – Source: https://github.com/pytorch/pytorch

2. TensorFlow – GitHub contributors: ~3,500+ – Monthly active contributors: ~200 – Core Maintainers: 70 -Users: ~2.5–3.5 million – Lead Developer: Google – Source: https://github.com/tensorflow/tensorflow

3. Hugging Face – GitHub contributors: ~2,600+ (Transformers repo) – Monthly active contributors: ~150 -Core Maintainers: 50 – Users: ~1.5–2.5 million – Source: https://github.com/huggingface/transformers

Global Ecosystem of Users

AI/ML Engineers (1.2M – 1.8M): Full-time professionals training and deploying models using programs provided by open source Academic Users (800K – 1.2M): Researchers, grad students, and educators who also train and deploy models Indie Devs & Hobbyists (400K – 700K): Kaggle participants, open-source users, startup tinkerers Enterprise Software Devs (3M – 5M): Developers integrating AI into enterprise apps

Industry Impact

• 75%+ of Fortune 500 companies use open-source AI directly or via cloud providers • Hugging Face Hub sees millions of downloads monthly (https://huggingface.co) • GitHub’s Octoverse consistently ranks PyTorch and TensorFlow among the top OSS projects (https://octoverse.github.com/)

Top AI Companies: Builders vs. Train & Deployers

Open Source Corporate Builders: • Meta (PyTorch, Llama) • Google (TensorFlow, JAX) • Microsoft (ONNX, DeepSpeed) • NVIDIA (CUDA, cuDNN, Triton) • OpenTeams (Nebari, PyTorch, TensorFlow) Note: these companies can also train and deploy models

Open Source Train & Deploy Companies: • Amazon, Apple, Salesforce, Oracle, Palantir, Snowflake, Databricks, C3.ai, SAP, OpenAI, Anthropic, xAI Note: both Mistral and Anthropic claim to have some internal building capabilities, but as closed-box systems it cannot be confirmed

Overpriced rounds, a late stage VC bubble, and Sarbanes-Oxley are killing VC, markets and founders, as well as worsening inequality by limiting middle-class access to growth investment companies.

Overpriced rounds, a late stage VC bubble, and Sarbanes-Oxley are killing VC, investors and founders, as well as worsening inequality.

Institutional Investment in Late-Stage Venture Capital: Navigating Perverse Market and Regulatory Dynamics

Institutional investors’ sustained interest in late-stage venture capital (VC) funds is shaped by a complex interplay of behavioral, economic, and regulatory factors, despite these funds often underperforming relative to benchmarks such as the S&P 500 (see part I of this series). In this part II, I’ll examine the impacts of psychological biases, economic incentives, regulatory changes, liquidity preferences, and the evolving market dynamics that drive institutional capital toward late-stage ventures regardless of cost.

Institutional investors are often drawn to late-stage funds and the companies they back due to perceived lower risk, attributable to their established business models and proximity to liquidity events like IPOs. There is a lot of bias and false beliefs built into this system, and it has become toxic. So let’s break down what’s going on, and why allocators are funding this way.

Psychological Biases and Market Dynamics

Behavioral finance principles, such as the familiarity principle, herd behavior and the sunk-cost fallacy, are extremely relevant to investment decisions and play an outsized role in decisions to invest in late vs. early stage VC funds. Let’s cover these first.

The familiarity principle ensures that the known quantities—established companies nearing an IPO—seem safer than less predictable early-stage investments, even if they don’t provide investment returns that are positive after risk adjustment relative to the S&P 500. Because you’ve heard the names Stripe, WeWork, OpenSea, Brex, you are inclined to invest in the thing you’re familiar with, and the funds that back them. That can be a bad assumption when WeWork is the one you back.

The perceived safety of herd behavior (AKA, the bandwagon effect), wherein institutions follow the investment leads of their peers, is misleading. The assumption that the crowd knows best can also be viewed as a fear of missing out on potentially profitable opportunities. No one gets fired for following the market, so playing it safe with the pack is a reasonable strategy. Unfortunately, this is how lemmings go off cliffs.

The sunk-cost fallacy is another cognitive bias that leads many allocators to continue investing in a fund because of the time, money, or effort they have already committed, rather than cutting their losses. The rationale is often that not continuing the investment would mean that the initial resources were wasted, even though continuing does not necessarily lead to a recovery of those sunk costs.

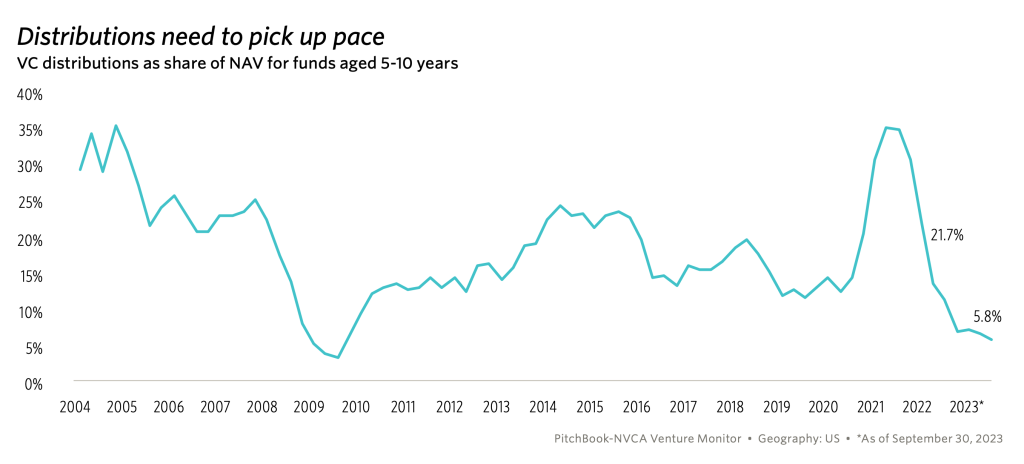

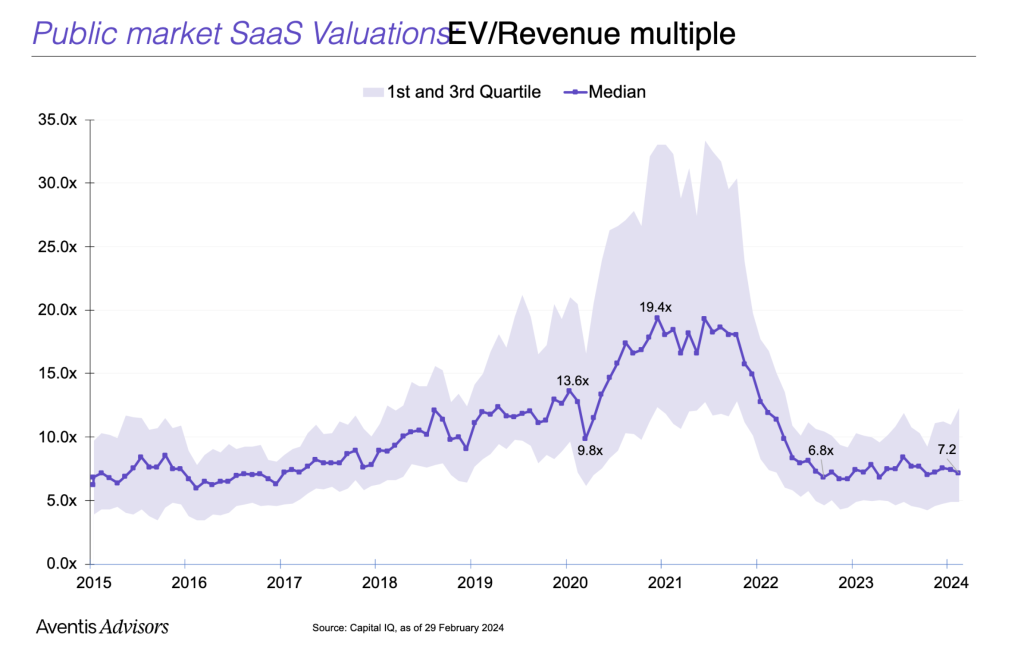

The combined effect of these three biases are beginning to be apparent when you examine flows of capital into late-stage VC funds, with LPs going along for a “ride” that seems stuck in neutral. Moreso, it may also be that allocators have lost the ability to underwrite technology, human resource, and execution risk, and are now only willing to underwrite market risk. Consider the following charts:

Distributions are at record low for a non-recessionary period, because overpriced deals over the past four years can’t be off-loaded to public markets. After pricing SaaS deals at 20x revenue just three years ago, you have a stupid amount of growth required to reach the same valuation at 7.2x revenue. Today’s valuation multiples aren’t low either, they are average for fundamental analysis based upon discounted cash flows weighted for a reasonable cost of capital in our current rate environment, unlikely to change and more realistic than the free money of the past decade.

As a result, late stage VC funds are writing larger checks to existing portfolio companies at higher and higher valuations to keep them afloat (if they’re still losing money) or in a ponzi scheme effort to keep over-marking up the winners to offset the losers. Worst of all, by delaying exits, they are not providing exit liquidity to their LPs and thus replenishing the VC funding cycle. According to JPMorgan in the Pitchbook NVCA 2023 Venture Monitor, “for vintage years 2013 to 2019, over 50% of the total value in venture funds relies on existing positions.”

Because late-stage VCs can’t IPO today without taking losses on their portfolio after writing big checks at massively inflated valuations, “unicorn” hold times increase beyond fund timelines.

What sustains this cycle is LPs willingness to keep pumping money into the late-stage funds so they can continue their sunk-cost fallacy investing on valuations not subject to public market scrutiny. Again, no one wants to recommend the “riskier” emerging manager at a small fund when the so-called experts at name brand funds are struggling to perform. Familiarity and herd bias alert!

As a result, early-stage VC is getting crowded out. The share of early-stage VC deals between $5-10mm has shrunk by 2/3. LP funds available for early-stage VCs continue to shrink. According to data from Crunchbase, 84% of capital raised by U.S. venture investors went into funds raising $250 million or more in 2018, and has increased every year since then according to Pitchbook data. As a result, VC funds managing $250m or less now account for less than half of all VC capital raised, down from over 75% in 2013. In the first two quarters of 2024, just two funds, Andresson-Horowitz and General Atlantic, raised 44% of all the venture capital raised by all VCs (Pitchbook).

While I have no data to support a hypothesis that allocators have lost the ability to underwrite technical, human resource, and execution risk, it’s clear that they are not underwriting these from the checks they’re giving VCs. Given that they only appear to be willing to invest in market risk, it seems bonkers that they do so without liquidity. You can better manage market risk in public equities with liquidity, so why do VC at all (and we’re back to part I).

This trend also shows in absolute dealmaking numbers collapsing for early-stage VC. According to AngelList, the second quarter of 2023 saw the lowest rate of early-stage startup dealmaking in the history of their dataset (dating back to 2013).

If you read part one of this series, the irony of the situation is that the VCs who continue to generate the highest returns are having the hardest trouble getting capital as late-stage VCs hoard assets and LP money. Until late-stage funds provide LPs liquidity via exits, the cash that feeds the whole ecosystem is locked up. Those exits are not likely to come soon.

Late stage VC is poisoning the well for the whole industry.

So why don’t early-stage VCs just work with founders to bypass the late-stage fiasco and encourage their portcos to go public after their series A/B rounds like we used to? Well, Congress kind of messed that up for everyone.

Impact of Regulatory Changes on IPO Timing

After the Enron scandal (which someday I’ll write a very cool post about but SoxLaw has an excellent summary here) Congress needed to show voters that they were going to do something about corporate fraud. In typical government action, they acted without fully considering the consequences of their actions. Surprise! Government is as ignorant as it is incompetent.

The resulting Sarbanes-Oxley Act of 2002 had a profound impact on the public offering landscape by dramatically increasing the cost to be a publicly traded company, imposing stricter financial reporting rules, forcing companies to hire more auditors to audit the audit (yes, that is as crazy as it sounds), and dramatically escalating governance standards for public companies.

In summary, Congress decided to stamp out fraud from corrupt auditors by adding even more auditors and creating additional byzantine governance systems for them and corrupt managers to hide in. Yes, that makes no sense.

I’ve looked at a lot of academic research to see if SOX actually reduced fraud. Without going into too much detail, it hasn’t. The best paper I can find on the topic shows that SOX only reduced the “probability” of fraud by about 1%. However, it did dramatically improve the detail of reporting provided to the public. Let’s not minimize that, and yet I’m hoping that Adam Packer will do a brilliant analysis to see if this resultes in improved investment manager performance -likely not, but surprise me!

So while SOX did dramatically improve information reporting and volume, fraud has not really decreased, valuations are down, and companies have to delay their IPOs due to increased costs and expanded public-listing responsibilities.

The average cost for SOX compliance is exploding. According to Protiviti’s annual SOX expense survey, on average, companies allocate $1–2 million for their SOX budget, with internal audit teams dedicating an additional 5,000–10,000 hours annually to SOX programs.

According to Protiviti, the average SOX compliance cost in 2023 was:

Companies with more than 10 locations: $1.6 million

Companies with only one location: $704,000

Companies with $10 billion or more in annual revenue: $1.8 million

Companies with $500 million or less in annual revenue: $651,000

When you have to shell out $1-2mm for one compliance cost, plus heaven-only-knows how many thousands of hours of additional internal audit time, you can’t go public until the economics make this massive cost immaterial.

As a result, since SOX passed, the average time from founding to IPO has notably increased—from about 5 years in the late 1990s to more than 10 years recently (Pitchbook data, thank you once again). This regulatory-induced delay significantly affects the liquidity of investments, particularly those made by early-stage venture funds, extending the time to potential returns.

So, getting liquid on VC investing is more expensive and takes longer than ever. These are the primary reasons late-stage VC is so attractive to LPs. Despite poor performance, institutional funds have a strong liquidity preference, even if the private markets aren’t beating the S&P 500 (again, see part I).

Liquidity Preferences of Institutional Investors

Given the extended timelines to IPOs, late-stage VC funds have become more attractive due to their shorter duration from investment to exit. While I can complain all day about extended unicorn hold times, the hold times are still longer if you invested earlier. Institutional investors, including pension funds and endowments, prefer investments that align with their liquidity timelines. Late-stage investments generally offer a quicker path to liquidity, matching the large pools of capital that institutional investors need to deploy efficiently.

So when average VC hold time is approaching ten years AFTER becoming a unicorn, who wants to invest in the early stage VC who backed them six to seven years before then (CB Insights, State of Venture 2023). Seventeen to twenty years is a very long time for an institutional LP to hold a private security, so who can blame them!

While I can find no solid economic research to explain why institutional investors would favor late stage VC on the basis of liquidity preferences alone, it stands to reason that a 17-year hold period is not acceptable for most funds of any size to get liquidity at any cost.

The Necessity of Large Capital Pools and the Impact on Founders

The growing average market cap of companies at IPO—from around $500 million in the early 1990s to over $2.5 billion today—requires larger rounds of late-stage funding. As companies grow larger and remain private longer, they need substantial capital to scale up to absorb the costs of a public offering post-SOX. This need makes large late-stage funds particularly appealing, as they are capable of mobilizing the capital required for continued growth. However, this trend has profound implications for startup founders, who often endure increased dilution and a loss of control as they raise more capital under increasingly stringent terms. The loss of control has real impact, as TechCrunch recently reported that VCs are using this power to block IPOs and prevent founders from liquidity. This leads to strategic misalignments that might endanger long-term success.

The assumption here by VCs justifying their control provisions is that the late-stage VC funds provide better oversight and governance and will better protect investor interests on behalf of their LPs. Really? Are VCs better and smarter than public markets and their oversight? I doubt it.

Again, I have no research (and I doubt you could put together a credible quantitative analysis), but I think it stands to reason that thousands of public investors and a public board of directors do a better job of oversight than a handful of privileged insiders who fundamentally share the same world-view as VCs. Yes, we have group-think and bias too, so better off if more eyes can see the business.

The closest thing I have to a benchmark on this is to see how company valuations change post-IPO, when public scrutiny provides the best check to the opinions of private company valuations and the ability of VCs to provide good oversight and valuation guidance. And yes, when you look at the sheer number of unicorns falling from grace since 2022, it would appear that the private markets overpriced and misgoverned significantly (see Techcrunch and Hurun).

A final note on this, if you want to nerd out on great IPO data, check out Jay Ritter’s recently updated data here. It rocks.

Diseconomies of Scale and Risks to the Ecosystem

The preference for large funds and substantial capital injections can lead to diseconomies of scale, where the size of the investments begins to detrimentally affect fund performance. As suitable investment opportunities become scarcer, funds may end up deploying capital in less optimal ventures, with more funds bidding up the price for available assets. This, in turn, can dilute returns. Moreover, as founders lose equity and control, the risk of misaligned interests increases, potentially affecting the company’s strategic decisions and long-term viability.

The larger the fund, the greater the challenge in deploying capital efficiently, which often results in decreased returns and increased risk of strategic misalignment within funded companies. Ouch.

Conclusion

Institutional investors’ preference for late-stage venture capital funding is dictated by a blend of psychological biases, regulatory impacts, liquidity preferences, the loss of their ability to underwrite anything except market risk, and the structural requirements of modern IPOs. While these investments may offer the perceived safety of shorter time horizons and reduced risk, they come with their own set of challenges, including potential misalignments and increased founder dilution.

The situation was made worse when the 2021-22 market bubble caused late-stage funds to overprice investments, and now extend exit periods so that they can avoid going public at a loss. Without exits, no new liquidity is flowing back into institutional and large family office LP investors, so early-stage VC funds are getting squeezed with fundraising for new funds that have ever elongating exit strategies. This, in-turn, creates less companies getting funded to their series A/B, and further restricting deal flow for late-stage funds, thus exacerbating their crisis to allocate capital and double down on their already overpriced, current portfolio companies.

So how do we break this doom-cycle? Part III coming soon…

Every VC fund needs a token, white, male, general partner.

Sputnik ATX does mark-to-market portfolio updates quarterly and the results thus far have been fantastic (89%IRR, not that I’m bragging). Our goal is to help people reach their full potential, and we believe that IRR is a key outcome to measure if we’re doing our jobs well. Diversity is another measure of that success. How are we doing?

Two metrics we’re just as proud to cite: over 40% of our portfolio companies have a female founder, and over 20% have a black founder. How do we do it? We joke among our team that our secret to success is maintaining a token, white, male, general partner.

Yes, I’m the only white dude.

The fact that we have only one white male on our team gives us an unfair advantage. I highly suggest more VCs try this approach. If you’re a general partner (GP) reading this article, please consider ways to get your own token, white, male GP and do so NOW.

What we’ve learned at Sputnik ATX is that when diverse people (education, culture, work experience, ethnicity, gender, etc) all have a say in decisions, we make FAR better decisions. There is copious research to support me on this (check out this HBR article.).

We’re well past the time to continue to allocate capital to homogeneous white dudes and yet, the flow of capital to these funds is shockingly disproportionate and persists. It’s time for lip service to end, and action to begin.

At the risk of alienating allocators looking at our next raise, I just have to say to every fund of fund manager and pension fund manager, please stop giving money to funds where the GPs all look like me. It’s hurting your returns, its skewing investment away from quality founders, its exacerbating US economic apartheid, and preventing everyone from reaching their full potential.

Note: I highly suggest reading the links in this article, and the book on US economic apartheid is especially interesting. Also, after writing this article, Sputnik ATX shockingly found another white guy who joined our team as a temp this summer. Congrats Matt, you beat the odds at our fund. Let’s not get too comfortable. Our investor returns depend on it.

It’s time America unites to fight our common enemy instead of one another.

At the dawn of World War II as Hitler rose to power and started militarizing Nazi Germany, UK Prime Minister, Neville Chamberlain, cut defense spending and engaged in a strategy of placating evil. Sure, historians debate the full extent of Chamberlain’s lack of vision, but his all but flat-out ignoring the threat of Hitler didn’t make the war go away. Today, Chamberlain is regarded as one of the worst PMs in UK history, and one of the leading factors no one checked Hitler’s rise to power earlier.

Enter COVID-19, and US President Donald Trump. We have a new invasion, and in the first year, it will likely kill over 200,000 Americans. World War II took the lives of just over 400,000 Americans, over a period of four years. In short, the war against COVID-19 is deadlier than World War II in its ability to kill Americans faster. And yet, here is the President of the United States, at first denying the risk, then when obvious wearing no mask, ordering testing to slow down, holding massive rallys-cum-super-spreader events, and asking people to ignore the obvious: we are at war. Neville Chamberlain couldn’t have done it better, I think Trump is using his playbook.

When Imperial Japan attacked the United States, a draft card was a sign of patriotism. Many courageous youth even lied about their age and health conditions to get into the fight. Healthy and able Americas were united in their desire to sacrifice whatever was required to protect those who couldn’t fight: E pluribus unum. Presidents and Prime Ministers of Allied forces asked for sacrifice, and a willing country united against a common enemy with patriotic ferver.

Back to COVID-19. Wearing a face mask is the draft card of this war. True patriots wear a face mask to protect Americans who can not protect themselves. Strong leaders care for those who are at risk, and many patriotic Americans wear masks in the great American tradition of doing whatever is required to protect those we love.

Sadly, despots and tyrants use propoganda at times of national crisis in an attempt to aggregate their power. The love of power, and the selfish exercise of power to harm the public good, is why our founding fathers created our democratic system. So that once every four years, we vote and make sure that our country is led by someone who puts others above themselves, in the best traditions of America.

Bring on America’s Winston Churchill. It’s time America unites to fight our common enemy instead of one another.

Bitcoin investors should learn a lesson from Awesome, a dictator who lost his life introducing the one of the world’s first fiat currencies

Bitcoin investors should learn a lesson from Awesome, a dictator who lost his life introducing the one of the world’s first fiat currencies. A fiat currency is a form of money to exchange goods and services that has no intrinsic value. For example, a gold coin is not a fiat currency, because it is made of gold, something that has value in, and of, itself. Paper currency, like the US Dollar, is a fiat currency because the note has no intrinsic value.

Bitcoin has a lot in common with early fiat currencies, so let’s take a second to review fiat currency and take a quick history lesson from one of its early adopters.

First off, how does fiat currency get its value? Fiat currency has value when:

1. It has limited supply

2. People believe it has value

3. It can be easily transferred to facilitate economic transactions

Right now, Bitcoin meets all three of these standards. There is limited supply due to its unique block-chain encryption standards, people believe it has value from the increasing rate of exchange to the dollar, and it can be transferred easily to facilitate economic transactions using online Bitcoin wallets. So how did fiat currencies get started and what can we learn from these early currencies about the future of Bitcoin?

In 1294 Gaykhatu (literally, “Awesome” in Mongolian) was the leader of one Hoard of Mongols ruling over what is now Iran, Iraq and Southwest Asia. Taking his name a little too literally, Awesome decided that he needed fiat currency like that introduced by his distant cousin Kublai in China.

Awesome was in the middle of a crippling drought in his territory, and after several years of expending all of the royal treasury building a seriously sweet palace (still unfinished, of course), he was broke. When he heard that Kublai was just printing his own money, he saw his path to riches and summoned the Ambassador from Kublai’s court, demanding to see the new paper currency.

So smitten with this idea, Awesome copied the idea and printed his own money. He liked the notes printed by Kublai so much, he even copied the Chinese characters on them. He demanded that everyone accept these new notes as currency. However; Awesome had competing currencies. He didn’t think about confiscating all the gold and silver currency in circulation and soon discovered that no one wanted his paper money (Kublai at was smart enough to make some of his Chao out of copper to help with the perception of value).

Awesome also launched his new currency during the worst cattle plague his realm had ever encountered, and printing new money at such a tumultuous economic event was just poor form. Needless to say, no one thought Awesome was awesome. Riots and violence broke out around his kingdom.

Topping it off, Awesome himself emptied out his treasury of the notes he printed for himself, buying lavish materials for his palace from merchants foolish enough to accept his worthless piles of paper. Awesome was bankrupt, his markets frozen from the lack of a credible medium of exchange.

In the end, he was pelted with all manner of foul, medieval produce without refrigeration, and openly mocked over the irony of his increasingly worthless name. His cousin was so angry, he didn’t stop there, he killed Awesome by strangulation with a bowstring and took over his kingdom. Yeah, that ended badly.

So, what does this have to do with Bitcoin? Bitcoin has value only from the drug dealers, money launderers, illegitimate governments, and black market moguls who see Bitcoin as a valuable exchange to conceal their dirty doings. Like Awesome, these neer-do-wells created a virtual currency that can’t be traced to support their palace building.

And like Awesome, this party will crash back down to earth. There are two primary structural problems to Bitcoin that will undermine its ability to satisfy all three standards for a fiat currency.

First, quantum computing stands to make any encryption 100% worthless in the next ten years. We are rapidly approaching a future where there will be no secrets stored on computers, because no computer can encrypt itself sufficiently to prevent a quantum computer from hacking any and all methods designed to protect it, end of story. This means that the encryption protecting Bitcoin itself, Bitcoin wallets, and any and all servers that are used to process and secure its ownership rights, will all be broken and worthless. This destroys the fundamental premise of value, to say the least. Goodbye limited supply!

Second, governments can block people from using Bitcoin as a measure of exchange. Why would they do this? Because Iran, North Korea, drug cartels, tax evaders, and money launderers are using Bitcoin to evade sanctions, bank laws, taxes, and pretty much violate every lawful economic law on the books. They are already starting to do so, in China and South Korea, and the impact of this on Bitcoin value is just beginning.

At the end of Bitcoin, no governments will allow an asset class that has a primary purpose to undermine the faith of their regulated, lawful financial system and allow untraceable and untaxable exchanges of value between two parties. In short, all these ICOs are a threat to the established global financial system, so the governments who created this system will not permit Bitcoin to stand. You can’t fight city hall, let alone every major world government.

When these governments begin to go to war against crypto-currencies in earnest, belief that Bitcoin has value will plummet, the ability to use it to exchange goods and services will evaporate, and its demise will be the latest chapter in fiat currency collapse. When this happens, I hope the Winklevoss twins have good security. I’d hate to see them go the way of Awesome.

Joe Merrill is an Austin-Texas based venture capitalist at Sputnik ATX and Linden Ventures. Follow his blog at http://www.econtrepreneur.com or on Twitter @Austin_VC

Warning: this blog post is about taxes. Taxes are an inherently boring topic, but useful if you want to understand something that will seriously impact your life. So, please read on if you want to learn the economics of what takes 40%-50% of your income. Otherwise, stop here and remain blissfully unaware.

There is a lot in the press these days complaining about the tax cut package passed by congress and signed by the President. Almost universally, the comments in the mainstream media have an agenda that appears to be almost perfectly tailored for the echo chamber created on each side of the aisle for the major news outlets’ political sponsors. However, a careful scrutiny of the history of US tax law (and tax rates) paints a very different picture of how these tax cuts will impact the United States insofar as its impact on the tax base and the demand-side of the economy.

While US tax law goes back to the very founding of the Republic and the tariff system created by Congress to fund it, personal income tax is a relatively new idea. Although there was a brief period from 1861 to 1872 where a personal income tax existed to help pay for the civil war, it wasn’t until the 16th Amendment was passed in 1913 that the government actually got the right to tax our incomes for the first time.

From 1913 until 1931 at the start of the great depression, the federal tax rate hovered at around 1.1% for the poorest families and while progressive (meaning wealthier families paid more than this), it was not punitive for rich people either, with 7% as the top bracket for people earning over $12mm a year in today’s dollars (adjusted for inflation).

However, from 1932 to 1941, Hoover and FDR had tax policies that, by any survey of the most liberal-minded economists, had disastrous results on the economy. Tax revenue in 1931 was 834mm USD. In June of 1932, Hoover decided that the worsening economy required government to start collecting more taxes to balance the budget. Hoover almost tripled the top rate from 25% to 63%, and the low rate increased from 1.1% to 4%.

The amazing result was that tax revenue fell from $834mm to $427mm in 1932. Why? Well, when you take money from people’s pockets, they have less to spend. Less spending results in less profits, and lower corporate tax collections (if companies are losing money, they don’t have profits to tax). This fell further by 1933, with a mere $353mm in taxes collected as the economy continued to shrink and the government took more and more of the pie for itself (a concept economists call crowding out). FDR raised them up to 76% when he took office (he raised the top rates to 76% by 1936) and unemployment spiked to 20%. By 1937, FDR realized that his efforts to spend money to lower unemployment were only partially successful. Unemployment was down to 15% but the government was spending huge amounts of money and creating large debts in the process.

So why did this happen? This has to do with the impact of taxes on the overall economy and the velocity of money. Since the government can only tax profits on money in circulation, the speed with which money moves around between firms in an economy have a major impact on taxes. For example, if our economy only had four companies, and each company has $100 a year in profit on $200 in sales, then the economy would have $800 in sales, and $400 in profit to share. However, if the government taxes 50% of that profit, there is $200 less money for the companies to share with the economy, and the economy will shrink. Now, think about how many times a single dollar is exchanged in a year between consumers and companies, and how each time the dollar is exchanged it creates a taxable event. More exchanges equals more taxes.

So if the government raises taxes very high, they reduce the number of taxable exchanges by the amount they took in taxes multiplied by the number of times those dollars would have been spent in a transaction. In short, the government is taking money so that it can’t be spent and then taxed. While I’m not calling for the abolition of taxes so that we’ll have economic stimulus, it is a good idea to understand that when taxes go up, the economy goes down by a multiple of that tax collected.

However, at the time of these tax increases during the great depression, some Keynesian economists (those who believe that government expenditure is key to stimulating the economy) were shocked because these New Deal tax increases were increasing unemployment and New Deal spending wasn’t improving the economy to compensate.

Government spending was just helping us to limp along while incurring huge debts in the process since demand for government program spending far outstripped taxes collected. Governments are like us, if they borrow a lot of money today, they will need more income in the future to pay off the debt and maintain their standard of living. Sadly for us, when governments need to increase their income, they must raise taxes (taxes are the only way they get money legitimately). So FDR decided to raise taxes again and again. By 1940, the upper rate for wage earners was 94% for upper income earners, and 23% for anyone earning more than $500 a year. Needless to say, the economy was so bad by this point, it took World War II to force dramatic changes in production and labor and end the depression. At the end of WWII, Truman decided to start cutting government spending and lower taxes beginning in 1945. Economists complained at the time that Truman was going to guarantee another depression, after all government spending is what they believed saved them from the depression getting worse, right? Actually, Truman’s decision restored accountability in the economy and the nation grew to full employment in very short order. Needless to say, the corporate tax rate was dropped from 90% to 38%, providing companies plenty of additional cash to grow and hire new workers. In a recent survey, 2/3 of all economists agree that FDRs policies made the great depression worse and enabled it to stick around for a long time.

What does that mean for us today? Well, during the Obama administration taxes went up, and so did regulation (a quiet form of taxation because it raises the cost of doing business). So despite the Federal Reserve pumping unprecidented amounts of money into the economy through quantitative easing, the velocity of money (over 10 before Obama was elected) fell to just over 5 when he left office.

So, if we are to fix this, we need to have policies that would lower taxes and lower regulation to a sensible level. Both would be good ideas, if your goal is to grow the US economy. So when I hear people opposed to both of these, regardless of their intentions, we need to recognize that they are advocating policies that hurt the financial future of America’s families.

That is why it is all the more important to have sensible people in government who can not only enact policies that help working class families, but are able to explain these policies in a way that unites the American people behind them. Alas, that last part is what both parties appear to be lacking these days: leadership.

Note: some nut job out there may construe (how, I don’t know) this article as some sort of tax advice and then think about suing me. I’m not a tax adviser, this is not tax advice, so don’t make any tax decisions from my article. And yes, this is proof positive that attorney’s can ruin our lives.

Want to be wealthier? Stop being a jerk-face to #women.

America has a multi-trillion dollar problem that just hit home for me. My daughter was sexually harassed by another student at school, and worse, the school didn’t protect her when they knew it was going on.

When examining why some economic agents like companies, churches and schools continue to protect sexual predators, I’ve come to realize that this problem is probably the single largest drag on the global economy (at least the largest I’ve ever seen) and that our legal system provides warped, perverse incentives that perpetuate this perversion. The cost to our society of this broken system is staggering. And yet society continues to look the other way to a situation that reminds me of the old story about the gardener and the rabbit. It goes something like this:

Once there was a gardener who woke up every morning to discover that a rabbit ate much of his crop the night before. He tried everything to get rid of it, but the clever rabbit eluded him night after night. Finally, in desperation, the gardener built a strong fence around his garden, even digging a portion underground, to keep the rabbit out. Supremely confident in his fine fence, he slept well that night, only to awake and discover that the rabbit ravaged his beautiful garden once again. He had fenced in the rabbit the day before.

Like the farmer, our tort laws regarding sexual harassment are fencing in the rabbit, and providing incentives to churches, schools and workplaces to protect harassers.

So, let’s look closer at the perverted incentives for schools, churches and companies (which I will call social agents). If a person commits sexual harassment, and if anyone at a social agent had any inkling that that person was a perv, then the social agent bears some liability for the perv’s actions since it was foreseeable that harassment would take place. However, social agents and individuals tend to want to see the best in people, so when perv’s do something pervy, we try to explain it as “we must have just misunderstood what he/she meant”. That is because we are nice.

Predators depend upon our kindness to do their dirty deeds. I’m not suggesting that we stop being nice, but I think how we respond to inappropriate behavior must change.

First, we need to speak up when boundaries are crossed and not care if we offend. If a man or woman in your office puts their hand on your back or shoulder, that is crossing the line. You don’t need to touch people to do most jobs, and should only do so when it is required as a part of your job description and, even then, minimize this as much as possible. There is no such thing as an OK sexual joke at the office (or at home for that matter). Grooming people by talking around the edges on mature subject matter is not subtle, it is blunt and we don’t like it. Stop doing it now. It’s time to grow up and start respecting people appropriately.

Second, in today’s Donald Trump school of management, tort laws provide cover to economic agents who pride themselves by saying that they are protecting innocent men from the wild accusations of an accuser when really, they are just protecting their bottom line. This encourages the victim blaming and cover-ups that we see in the news every freakin’ day. Current tort law “fences in the rabbit”, by providing companies legal incentives to align with predators to fight off harassment claims to avoid paying damages. Instead, we need to look at the REAL damages.

Social agents incorrectly assume that the biggest harassment cost they need to avoid is financial damage from lawsuits. This false belief encourages them to deny harassment claims and fend off harassment accusations with no thought to the emotional and personal cost to the victims. In fact, the far bigger expense is the economic loss of productivity and the broken lives of their employees, investors and customers due to their policies that fence in rabbits.

At the macroeconomic level, ranges of the GDP cost due to gender discrimination and harassment vary between 10% and 25%. Given that global GDP is around 78 trillion dollars, we’re talking about 8 to 20 trillion dollars in lost global income creation each year due to harassment and discrimination. In contrast, we fret about the billions of dollars we spend defending lawsuits from harassment. Our priorities are wrong.

Social agents only hedge these defensive costs with defensive expenditure: insurance coverage, harassment training for employees, lawsuit settlements and, if they’re super progressive, on-site counselors to help those affected by sexual harassment. However, I believe that the best defense is a good offense. Let’s do something to get the 20 trillion dollars, please.

I would like to call upon our elected officials to pass new tort laws to permit and encourage persons sexually harassed to work with social agents to pursue justice against sexual predators together. This can be done by permitting and encouraging churches, schools, and companies to sue their students and employees who harass, and recover damages commensurate with the social cost, the total social cost -not just the defensive expenses. It is time for pervs to pay up or smart up. In this way, social agents have an economic incentive to identify and root out sexual harassment because they will share the benefit of legal actions against those who harass. Harassers have an incentive to change their behavior, and the homes that foster future harassers have economic losses to incentivize them to change their ways.

What I hope you now understand is that sexual harassment is an economically expensive epidemic, and the emotional and psychological cost to our wives, daughters, and girlfriends is incalculably higher. So, let’s shift that expense to those who create it, and make it possible for our churches, schools and companies to recover damages from those who create the problems.

When groping results in the loss of your parents 401(k), maybe parents, clergy and managers will stop saying, “boys will be boys”, excusing Trumpian “locker room banter” and begin teaching proper respect for women. Furthermore, suing predators will become an effective way for social agents to capture the expenses they bear to treat harassment victims who often require special accommodation to cope with school and the PTSD or other problems harassment creates in their lives. Better yet, maybe my daughters will be able to live in a world where their contributions are valued by society and they can live without fear.

Furthermore, when we replace faux corporate hand-wringing and cringing with “ka-ching” whenever a crude joke is told in the office, and the offenders lose real money to their employers, people will stop telling crude jokes, putting inappropriate hands on backs, grooming victims and doing other macro-aggressions. No one is trying to stop appropriately asking out a coworker on a date, it just needs to be done the right way, don’t be a perv.

In short, it is time we make harassment the problem of the perpetrators, and enable our social institutions to go after them to the economic and emotional benefit of all. Enough is enough.