The exit constipation in the VC world stems from market regulations, not bad actors. Founders often misjudge valuation premiums offered by mega-VCs, which favor the investors. Exploring IPOs in London and Toronto can restore liquidity and allow average investors access to growth equity, improving the global economy and potentially reforming US regulations.

For those of you who are skipping to the good part (and this is the good part), you really should take a moment to go back and see how we got here (Part I, Part II).

Because there are no bad actors driving the exit constipation in the VC world, just rational economic agents doing what market deforming regulations demand. But, now that we’re here, in an exitless void, here’s how we get out of it, and save VC as an asset class in the process. This is the new path to liquidity.

When taking money from mega-VCs, GPs seduce founders with what is typically a 10%-15% premium to the market from a valuation perspective. I know this from countless discussions with the partners, principals and associates that work at these funds over many, many years. That did change between 2020-2023 during the private bubble peak, but we’ve discussed how dangerous this was for different reasons in part I and part II.

When offered a premium to the market, it is deceptively easy to take the deal and feel like you’re getting a bargain as a founder. However, founders who lack formal financial training do not realize that they are comparing a premium on common shares to the preferred shares that VCs demand. These are not the same.

As pretty much every 409(a) document attests to, these preferred shares generally command a 30% premium to common shares. In short, the 10%-15% perception of overvaluation is, in fact, a 15%-20% discount in favor of the VC.

This is why I started recommending to all our portfolio companies to begin exploring exits beyond the reach of Sarbanes-Oxley, and explore IPOs in London and Toronto. This is the new way forward.

London and Toronto have deep markets (especially deep in London) where founders can IPO after a series A or series B and get to liquidity for themselves and investors in 5-7 years, thus escaping the madness of the great VC constipation crisis. By so doing, they also make employees liquid for option pools, access better governance and oversight, as well as access to capital that can further their growth without giving up preferred share premiums.

In return, average mom and pop investors will get access to growth company stock, just like they used to prior to the whole Enron/SoX fiasco.

This is actually an important structural fix for our global economy, restoring access to higher returns to average folks, where today only the wealthy get access to companies in the growth phase through private holdings.

Exiting via London, Singapore, Toronto, Riyadh, and other viable options is not just a better economic decision, it is the moral choice for the good of humanity any way you slice it.

If more companies went public when they first became a unicorn (or even before then), then VC would go back to funding seed and series A like they used to, with some series B for good measure. There would be no market for series C because public markets have way more liquidity than Sand Hill Road could ever dream of.

Another potential outcome to fix this would be if the US Congress amended Sarbanes-Oxley so that companies with valuations less than $1bn were only subject to audit requirements, like in the old days. With a modified but lighter version for companies with market caps between $2bn and $10bn, with full SOX after that. If the US adopted this model, we’d be competitive with other countries that realized their error and fixed this mess.

Until then, I think we’ll see US equity markets continue to yield market-share to foreign markets with less liquidity, and the great VC extension will continue.

Overpriced rounds, a late stage VC bubble, and Sarbanes-Oxley are killing VC, markets and founders, as well as worsening inequality by limiting middle-class access to growth investment companies.

Overpriced rounds, a late stage VC bubble, and Sarbanes-Oxley are killing VC, investors and founders, as well as worsening inequality.

Institutional Investment in Late-Stage Venture Capital: Navigating Perverse Market and Regulatory Dynamics

Institutional investors’ sustained interest in late-stage venture capital (VC) funds is shaped by a complex interplay of behavioral, economic, and regulatory factors, despite these funds often underperforming relative to benchmarks such as the S&P 500 (see part I of this series). In this part II, I’ll examine the impacts of psychological biases, economic incentives, regulatory changes, liquidity preferences, and the evolving market dynamics that drive institutional capital toward late-stage ventures regardless of cost.

Institutional investors are often drawn to late-stage funds and the companies they back due to perceived lower risk, attributable to their established business models and proximity to liquidity events like IPOs. There is a lot of bias and false beliefs built into this system, and it has become toxic. So let’s break down what’s going on, and why allocators are funding this way.

Psychological Biases and Market Dynamics

Behavioral finance principles, such as the familiarity principle, herd behavior and the sunk-cost fallacy, are extremely relevant to investment decisions and play an outsized role in decisions to invest in late vs. early stage VC funds. Let’s cover these first.

The familiarity principle ensures that the known quantities—established companies nearing an IPO—seem safer than less predictable early-stage investments, even if they don’t provide investment returns that are positive after risk adjustment relative to the S&P 500. Because you’ve heard the names Stripe, WeWork, OpenSea, Brex, you are inclined to invest in the thing you’re familiar with, and the funds that back them. That can be a bad assumption when WeWork is the one you back.

The perceived safety of herd behavior (AKA, the bandwagon effect), wherein institutions follow the investment leads of their peers, is misleading. The assumption that the crowd knows best can also be viewed as a fear of missing out on potentially profitable opportunities. No one gets fired for following the market, so playing it safe with the pack is a reasonable strategy. Unfortunately, this is how lemmings go off cliffs.

The sunk-cost fallacy is another cognitive bias that leads many allocators to continue investing in a fund because of the time, money, or effort they have already committed, rather than cutting their losses. The rationale is often that not continuing the investment would mean that the initial resources were wasted, even though continuing does not necessarily lead to a recovery of those sunk costs.

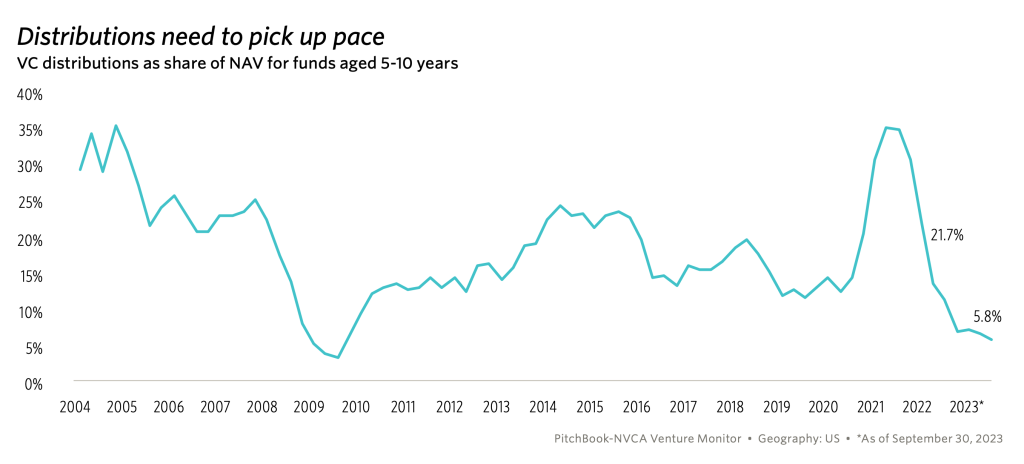

The combined effect of these three biases are beginning to be apparent when you examine flows of capital into late-stage VC funds, with LPs going along for a “ride” that seems stuck in neutral. Moreso, it may also be that allocators have lost the ability to underwrite technology, human resource, and execution risk, and are now only willing to underwrite market risk. Consider the following charts:

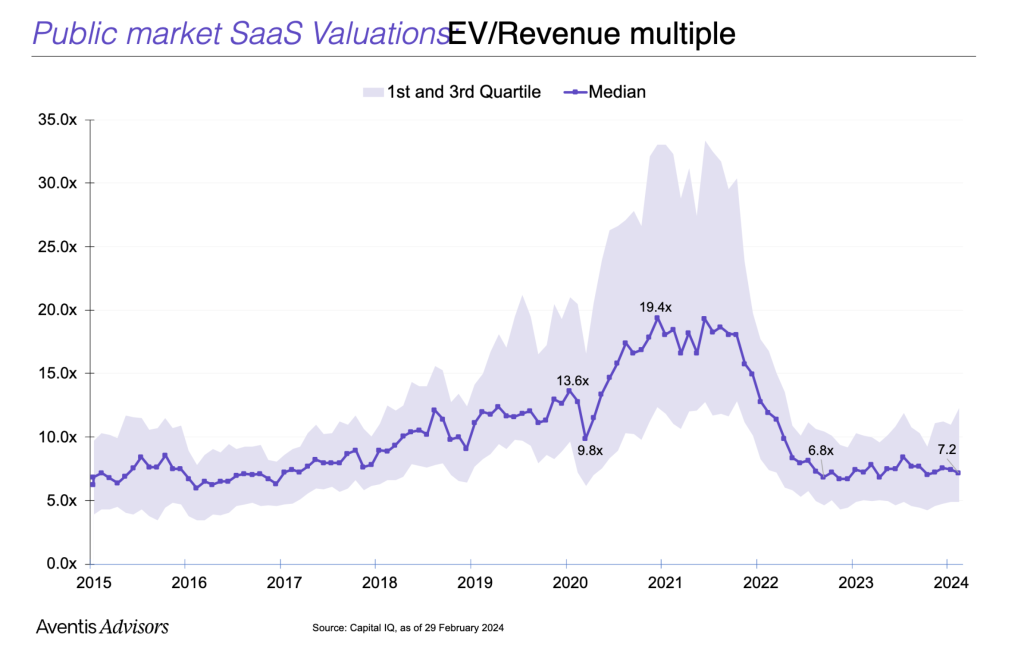

Distributions are at record low for a non-recessionary period, because overpriced deals over the past four years can’t be off-loaded to public markets. After pricing SaaS deals at 20x revenue just three years ago, you have a stupid amount of growth required to reach the same valuation at 7.2x revenue. Today’s valuation multiples aren’t low either, they are average for fundamental analysis based upon discounted cash flows weighted for a reasonable cost of capital in our current rate environment, unlikely to change and more realistic than the free money of the past decade.

As a result, late stage VC funds are writing larger checks to existing portfolio companies at higher and higher valuations to keep them afloat (if they’re still losing money) or in a ponzi scheme effort to keep over-marking up the winners to offset the losers. Worst of all, by delaying exits, they are not providing exit liquidity to their LPs and thus replenishing the VC funding cycle. According to JPMorgan in the Pitchbook NVCA 2023 Venture Monitor, “for vintage years 2013 to 2019, over 50% of the total value in venture funds relies on existing positions.”

Because late-stage VCs can’t IPO today without taking losses on their portfolio after writing big checks at massively inflated valuations, “unicorn” hold times increase beyond fund timelines.

What sustains this cycle is LPs willingness to keep pumping money into the late-stage funds so they can continue their sunk-cost fallacy investing on valuations not subject to public market scrutiny. Again, no one wants to recommend the “riskier” emerging manager at a small fund when the so-called experts at name brand funds are struggling to perform. Familiarity and herd bias alert!

As a result, early-stage VC is getting crowded out. The share of early-stage VC deals between $5-10mm has shrunk by 2/3. LP funds available for early-stage VCs continue to shrink. According to data from Crunchbase, 84% of capital raised by U.S. venture investors went into funds raising $250 million or more in 2018, and has increased every year since then according to Pitchbook data. As a result, VC funds managing $250m or less now account for less than half of all VC capital raised, down from over 75% in 2013. In the first two quarters of 2024, just two funds, Andresson-Horowitz and General Atlantic, raised 44% of all the venture capital raised by all VCs (Pitchbook).

While I have no data to support a hypothesis that allocators have lost the ability to underwrite technical, human resource, and execution risk, it’s clear that they are not underwriting these from the checks they’re giving VCs. Given that they only appear to be willing to invest in market risk, it seems bonkers that they do so without liquidity. You can better manage market risk in public equities with liquidity, so why do VC at all (and we’re back to part I).

This trend also shows in absolute dealmaking numbers collapsing for early-stage VC. According to AngelList, the second quarter of 2023 saw the lowest rate of early-stage startup dealmaking in the history of their dataset (dating back to 2013).

If you read part one of this series, the irony of the situation is that the VCs who continue to generate the highest returns are having the hardest trouble getting capital as late-stage VCs hoard assets and LP money. Until late-stage funds provide LPs liquidity via exits, the cash that feeds the whole ecosystem is locked up. Those exits are not likely to come soon.

Late stage VC is poisoning the well for the whole industry.

So why don’t early-stage VCs just work with founders to bypass the late-stage fiasco and encourage their portcos to go public after their series A/B rounds like we used to? Well, Congress kind of messed that up for everyone.

Impact of Regulatory Changes on IPO Timing

After the Enron scandal (which someday I’ll write a very cool post about but SoxLaw has an excellent summary here) Congress needed to show voters that they were going to do something about corporate fraud. In typical government action, they acted without fully considering the consequences of their actions. Surprise! Government is as ignorant as it is incompetent.

The resulting Sarbanes-Oxley Act of 2002 had a profound impact on the public offering landscape by dramatically increasing the cost to be a publicly traded company, imposing stricter financial reporting rules, forcing companies to hire more auditors to audit the audit (yes, that is as crazy as it sounds), and dramatically escalating governance standards for public companies.

In summary, Congress decided to stamp out fraud from corrupt auditors by adding even more auditors and creating additional byzantine governance systems for them and corrupt managers to hide in. Yes, that makes no sense.

I’ve looked at a lot of academic research to see if SOX actually reduced fraud. Without going into too much detail, it hasn’t. The best paper I can find on the topic shows that SOX only reduced the “probability” of fraud by about 1%. However, it did dramatically improve the detail of reporting provided to the public. Let’s not minimize that, and yet I’m hoping that Adam Packer will do a brilliant analysis to see if this resultes in improved investment manager performance -likely not, but surprise me!

So while SOX did dramatically improve information reporting and volume, fraud has not really decreased, valuations are down, and companies have to delay their IPOs due to increased costs and expanded public-listing responsibilities.

The average cost for SOX compliance is exploding. According to Protiviti’s annual SOX expense survey, on average, companies allocate $1–2 million for their SOX budget, with internal audit teams dedicating an additional 5,000–10,000 hours annually to SOX programs.

According to Protiviti, the average SOX compliance cost in 2023 was:

Companies with more than 10 locations: $1.6 million

Companies with only one location: $704,000

Companies with $10 billion or more in annual revenue: $1.8 million

Companies with $500 million or less in annual revenue: $651,000

When you have to shell out $1-2mm for one compliance cost, plus heaven-only-knows how many thousands of hours of additional internal audit time, you can’t go public until the economics make this massive cost immaterial.

As a result, since SOX passed, the average time from founding to IPO has notably increased—from about 5 years in the late 1990s to more than 10 years recently (Pitchbook data, thank you once again). This regulatory-induced delay significantly affects the liquidity of investments, particularly those made by early-stage venture funds, extending the time to potential returns.

So, getting liquid on VC investing is more expensive and takes longer than ever. These are the primary reasons late-stage VC is so attractive to LPs. Despite poor performance, institutional funds have a strong liquidity preference, even if the private markets aren’t beating the S&P 500 (again, see part I).

Liquidity Preferences of Institutional Investors

Given the extended timelines to IPOs, late-stage VC funds have become more attractive due to their shorter duration from investment to exit. While I can complain all day about extended unicorn hold times, the hold times are still longer if you invested earlier. Institutional investors, including pension funds and endowments, prefer investments that align with their liquidity timelines. Late-stage investments generally offer a quicker path to liquidity, matching the large pools of capital that institutional investors need to deploy efficiently.

So when average VC hold time is approaching ten years AFTER becoming a unicorn, who wants to invest in the early stage VC who backed them six to seven years before then (CB Insights, State of Venture 2023). Seventeen to twenty years is a very long time for an institutional LP to hold a private security, so who can blame them!

While I can find no solid economic research to explain why institutional investors would favor late stage VC on the basis of liquidity preferences alone, it stands to reason that a 17-year hold period is not acceptable for most funds of any size to get liquidity at any cost.

The Necessity of Large Capital Pools and the Impact on Founders

The growing average market cap of companies at IPO—from around $500 million in the early 1990s to over $2.5 billion today—requires larger rounds of late-stage funding. As companies grow larger and remain private longer, they need substantial capital to scale up to absorb the costs of a public offering post-SOX. This need makes large late-stage funds particularly appealing, as they are capable of mobilizing the capital required for continued growth. However, this trend has profound implications for startup founders, who often endure increased dilution and a loss of control as they raise more capital under increasingly stringent terms. The loss of control has real impact, as TechCrunch recently reported that VCs are using this power to block IPOs and prevent founders from liquidity. This leads to strategic misalignments that might endanger long-term success.

The assumption here by VCs justifying their control provisions is that the late-stage VC funds provide better oversight and governance and will better protect investor interests on behalf of their LPs. Really? Are VCs better and smarter than public markets and their oversight? I doubt it.

Again, I have no research (and I doubt you could put together a credible quantitative analysis), but I think it stands to reason that thousands of public investors and a public board of directors do a better job of oversight than a handful of privileged insiders who fundamentally share the same world-view as VCs. Yes, we have group-think and bias too, so better off if more eyes can see the business.

The closest thing I have to a benchmark on this is to see how company valuations change post-IPO, when public scrutiny provides the best check to the opinions of private company valuations and the ability of VCs to provide good oversight and valuation guidance. And yes, when you look at the sheer number of unicorns falling from grace since 2022, it would appear that the private markets overpriced and misgoverned significantly (see Techcrunch and Hurun).

A final note on this, if you want to nerd out on great IPO data, check out Jay Ritter’s recently updated data here. It rocks.

Diseconomies of Scale and Risks to the Ecosystem

The preference for large funds and substantial capital injections can lead to diseconomies of scale, where the size of the investments begins to detrimentally affect fund performance. As suitable investment opportunities become scarcer, funds may end up deploying capital in less optimal ventures, with more funds bidding up the price for available assets. This, in turn, can dilute returns. Moreover, as founders lose equity and control, the risk of misaligned interests increases, potentially affecting the company’s strategic decisions and long-term viability.

The larger the fund, the greater the challenge in deploying capital efficiently, which often results in decreased returns and increased risk of strategic misalignment within funded companies. Ouch.

Conclusion

Institutional investors’ preference for late-stage venture capital funding is dictated by a blend of psychological biases, regulatory impacts, liquidity preferences, the loss of their ability to underwrite anything except market risk, and the structural requirements of modern IPOs. While these investments may offer the perceived safety of shorter time horizons and reduced risk, they come with their own set of challenges, including potential misalignments and increased founder dilution.

The situation was made worse when the 2021-22 market bubble caused late-stage funds to overprice investments, and now extend exit periods so that they can avoid going public at a loss. Without exits, no new liquidity is flowing back into institutional and large family office LP investors, so early-stage VC funds are getting squeezed with fundraising for new funds that have ever elongating exit strategies. This, in-turn, creates less companies getting funded to their series A/B, and further restricting deal flow for late-stage funds, thus exacerbating their crisis to allocate capital and double down on their already overpriced, current portfolio companies.

So how do we break this doom-cycle? Part III coming soon…

Late stage VC funds are earning dismal returns relative to the S&P 500 and take little risk. So why are LPs continuing to fund them? What the heck is happening in VC and can we fix it?

Welcome to the world of unlevered, illiquid, venture investing!

In this bizarro world, bigger is worse, and investors don’t seem to care.

What is going on?

Part One of a Three Part Series

Venture Capital Returns by Fund Size: Comparing Early-Stage vs. Later-Stage

Venture capital (VC) is a critical component of the financial landscape, fueling innovation and growth within the startup ecosystem. However, the returns on venture capital investments can vary significantly based on several factors, including the stage of investment and the size of the fund. Without trying to boil the ocean, I’m going to do a quick look at how venture capital returns diverge by fund size, with a specific focus on comparing early-stage and later-stage VC investments. Additionally, I want to cover how early-stage funds, particularly those smaller than $250 million, often outperform their larger counterparts, especially when compared against broader market benchmarks like the S&P 500.

Venture capital funds are typically classified into different stages based on the maturity and revenue of the companies they invest in: early-stage (Seed and Series A), mid-stage (Series B and C), and later-stage (pre-IPO financing). The size of these funds can also vary, ranging from small funds (less than $250 million) to large funds (more than $1 billion).

Later-Stage VC: Higher Risk with Lower Relative Returns Relative to Early Stage VC

Later-stage venture investments involve funding more established companies that are closer to a public offering or a major liquidity event. These investments are perceived as less risky compared to early-stage investments because the companies have proven business models and steady revenue streams. However, the return on later-stage investments can be less attractive compared to early-stage investments on a risk-adjusted basis. According to data from Cambridge Associates, later-stage VC funds have demonstrated lower returns compared to early-stage funds. The 10-year pooled return for later-stage funds as of 2020 was around 12%, significantly lower than the returns generated from early-stage funds which averaged around 20% (1). I’m looking for more recent data, because I’d bet my bacon that late stage fund returns went down, a lot, on average. At least, that’s what institutional LPs tell me, a lot. So much so, I wonder why they keep investing (that is part II of this essay).

Moreover, when comparing these returns to the S&P 500, which delivered a historical average annual return of approximately 8% to 10% with considerable liquidity, the attractiveness of later-stage VC diminishes further. The lack of liquidity and higher relative risk associated with late-stage venture investments, combined with returns that do not commensurately reward this increased risk profile, makes them less appealing compared to other investment opportunities. And yet, late stage VC keeps on raising money, lots and lots of money.

Early-stage venture capital involves investing in startups at their nascent stages, typically while their revenues are $3mm a year or less. These investments are inherently riskier due to the unproven nature of the businesses and their higher likelihood of failure. However, the potential for high returns is significant, especially for top-performing funds. A pivotal study by Cambridge Associates shows that top decile early-stage venture capital funds, particularly those with under $250 million in assets, have significantly outperformed their larger counterparts and broader market indices. The top decile of early-stage funds reported returns as high as 35%, showcasing exceptional performance that should attract sophisticated investors (2).

This performance variance can be attributed to several factors. Smaller early-stage funds are often more agile, able to make quick decisions, and invest in innovative startups that larger funds might overlook. Additionally, these smaller funds can provide more hands-on support to their portfolio companies, contributing to their chances of success.

That’s where early-stage VCs can generate massive alpha, and late stage simply can not because the companies are already significantly de-risked. Risk equals reward, and those who manage risk better, can earn returns in excess of their risk adjusted expectation. Later stage VCs require less risk-management ability, and their relatively poor returns reflect this.

Comparative Analysis with the S&P 500

When compared to the S&P 500, top-performing early-stage venture capital funds offer much higher returns, albeit with greater volatility and liquidity risk. For investors, this trade-off is often acceptable due to the substantial premiums involved. According to the National Venture Capital Association, early-stage funds not only surpass the S&P 500 in terms of returns but also contribute significantly to job creation and technological advancements, thereby offering both financial and societal benefits (3).

Part II Teaser

In summary, while venture capital as an asset class can offer high returns, the variability of these returns based on the stage of investment and the size of the fund is significant. Later-stage venture capital, despite its lower risk profile relative to early-stage investments, often fails to provide returns that justify the risks and illiquidity involved. Conversely, smaller early-stage funds, particularly those making Seed and Series A investments, consistently outperform not only their later-stage counterparts but also the broader market indices like the S&P 500 when considering top decile performers. These findings underscore the importance of strategic fund selection based on detailed performance data and fund characteristics in the venture capital industry.

So how did we get here? Why are LPs piling into bigger and bigger funds that offer returns lower, and lower each year? This makes even less sense when we consider that the S&P has been recently beating late stage VC returns, WITH LIQUIDITY!!!

【1】Cambridge Associates, US Venture Capital Index and Selected Benchmark Statistics 【2】Cambridge Associates, US Venture Capital Index 【3】National Venture Capital Association, 2020 Yearbook

The beauty and promise of cryptocurrency is that Bitcoin and Etherium truly became the worlds first fiat monies divorced from any government backing. Yes, use of fiat is blasphemy to crypto die-hards, but for crypto currency to succeed as a global currency, we need to have an honest conversation about what fiat really means, and how crypto must kill off it’s government independence if it wants to truly reach its full potential.

Fiat currency is a medium of exchange that has no intrinsic value, unlike gold and other precious metals, that have industrial and artistic use with value apart from its circulation as money. Fiat currency has value because we believe it has value, and thus becomes a store of value and medium of exchange. Fiat currency to an economist is money that only has value because we have faith in it, and it has no use otherwise.

In this way, crypto currencies are true Fiat monetary systems in a pure way. Divorced from any government backing, and with an alternative use case of zippo, they truly are a medium of exchange that is divorced from everything. And therein lies the rub.

Governments hate stuff they can’t control. And Bitcoin/Etherium are far from their reach. The Satoshi’s and Buterin’s of crypto built their systems in such a way that governments can never, ever control them. And that is beautiful when it comes to creating the perfect fiat currency. No more printing money when you need it (looking at you Zimbabwe), and all the other money mischief devised by central banks that protect governments and hurt everyday people (for a good read on the various ways governments have done this, Milton Friedman has a great read by the same title if you click the link).

Governments have thus far reacted to crypto with what John Gottman recognized as one of the ultimate forms of rejection and contempt: stonewalling. This is when you just go quiet. Say nothing. Sit still. Ignore. The epic lack of regulatory interest in crypto is accomplishing its purpose: killing crypto silently.

Crypto currency’s promise, to have a stable system of exchanging stuff divorced from government mayhem, will never be realized until governments learn to accept that the future of currency is out of their control, but within their regulation. And this is where crypto lovers weep: regulation must happen for crypto to reach its full potential. In this way, crypto dies so that it can live.

In a world where we buy stuff and pay our taxes in Bitcoin and Ethereum, governments need to have rules around how money can be used. These rules include how to get paid back if you’re ripped off, how to track money to protect us from dark forces, and how to make sure people aren’t manipulating crypto markets and hurting consumers by restricting supply and demand. The public benefits of crypto currency are many, but only if the beast is trained to avoid destroying our freedom with its own.

And here lies the root cause of our current dilemma. A US Congress so old it might as well be a nursing home, led the way with the oldest White House leader ever, means that US leaders are too far removed in history to address modern problems they do not understand. Joe Biden remembers world war two as a kid. Ponder that and honestly ask yourself if he’s ready to suggest ways government can adopt the future of money. Yeah, I didn’t think he was doing anything either.

What the world needs right now is visionary leadership from a new generation of forward-thinking monetary leaders. Sadly, I’m not sure we have them right now, at least not outside of the developer community. Ouch.

Bitcoin investors should learn a lesson from Awesome, a dictator who lost his life introducing the one of the world’s first fiat currencies

Bitcoin investors should learn a lesson from Awesome, a dictator who lost his life introducing the one of the world’s first fiat currencies. A fiat currency is a form of money to exchange goods and services that has no intrinsic value. For example, a gold coin is not a fiat currency, because it is made of gold, something that has value in, and of, itself. Paper currency, like the US Dollar, is a fiat currency because the note has no intrinsic value.

Bitcoin has a lot in common with early fiat currencies, so let’s take a second to review fiat currency and take a quick history lesson from one of its early adopters.

First off, how does fiat currency get its value? Fiat currency has value when:

1. It has limited supply

2. People believe it has value

3. It can be easily transferred to facilitate economic transactions

Right now, Bitcoin meets all three of these standards. There is limited supply due to its unique block-chain encryption standards, people believe it has value from the increasing rate of exchange to the dollar, and it can be transferred easily to facilitate economic transactions using online Bitcoin wallets. So how did fiat currencies get started and what can we learn from these early currencies about the future of Bitcoin?

In 1294 Gaykhatu (literally, “Awesome” in Mongolian) was the leader of one Hoard of Mongols ruling over what is now Iran, Iraq and Southwest Asia. Taking his name a little too literally, Awesome decided that he needed fiat currency like that introduced by his distant cousin Kublai in China.

Awesome was in the middle of a crippling drought in his territory, and after several years of expending all of the royal treasury building a seriously sweet palace (still unfinished, of course), he was broke. When he heard that Kublai was just printing his own money, he saw his path to riches and summoned the Ambassador from Kublai’s court, demanding to see the new paper currency.

So smitten with this idea, Awesome copied the idea and printed his own money. He liked the notes printed by Kublai so much, he even copied the Chinese characters on them. He demanded that everyone accept these new notes as currency. However; Awesome had competing currencies. He didn’t think about confiscating all the gold and silver currency in circulation and soon discovered that no one wanted his paper money (Kublai at was smart enough to make some of his Chao out of copper to help with the perception of value).

Awesome also launched his new currency during the worst cattle plague his realm had ever encountered, and printing new money at such a tumultuous economic event was just poor form. Needless to say, no one thought Awesome was awesome. Riots and violence broke out around his kingdom.

Topping it off, Awesome himself emptied out his treasury of the notes he printed for himself, buying lavish materials for his palace from merchants foolish enough to accept his worthless piles of paper. Awesome was bankrupt, his markets frozen from the lack of a credible medium of exchange.

In the end, he was pelted with all manner of foul, medieval produce without refrigeration, and openly mocked over the irony of his increasingly worthless name. His cousin was so angry, he didn’t stop there, he killed Awesome by strangulation with a bowstring and took over his kingdom. Yeah, that ended badly.

So, what does this have to do with Bitcoin? Bitcoin has value only from the drug dealers, money launderers, illegitimate governments, and black market moguls who see Bitcoin as a valuable exchange to conceal their dirty doings. Like Awesome, these neer-do-wells created a virtual currency that can’t be traced to support their palace building.

And like Awesome, this party will crash back down to earth. There are two primary structural problems to Bitcoin that will undermine its ability to satisfy all three standards for a fiat currency.

First, quantum computing stands to make any encryption 100% worthless in the next ten years. We are rapidly approaching a future where there will be no secrets stored on computers, because no computer can encrypt itself sufficiently to prevent a quantum computer from hacking any and all methods designed to protect it, end of story. This means that the encryption protecting Bitcoin itself, Bitcoin wallets, and any and all servers that are used to process and secure its ownership rights, will all be broken and worthless. This destroys the fundamental premise of value, to say the least. Goodbye limited supply!

Second, governments can block people from using Bitcoin as a measure of exchange. Why would they do this? Because Iran, North Korea, drug cartels, tax evaders, and money launderers are using Bitcoin to evade sanctions, bank laws, taxes, and pretty much violate every lawful economic law on the books. They are already starting to do so, in China and South Korea, and the impact of this on Bitcoin value is just beginning.

At the end of Bitcoin, no governments will allow an asset class that has a primary purpose to undermine the faith of their regulated, lawful financial system and allow untraceable and untaxable exchanges of value between two parties. In short, all these ICOs are a threat to the established global financial system, so the governments who created this system will not permit Bitcoin to stand. You can’t fight city hall, let alone every major world government.

When these governments begin to go to war against crypto-currencies in earnest, belief that Bitcoin has value will plummet, the ability to use it to exchange goods and services will evaporate, and its demise will be the latest chapter in fiat currency collapse. When this happens, I hope the Winklevoss twins have good security. I’d hate to see them go the way of Awesome.

Joe Merrill is an Austin-Texas based venture capitalist at Sputnik ATX and Linden Ventures. Follow his blog at http://www.econtrepreneur.com or on Twitter @Austin_VC